This website uses third-party cookies to collect statistical information related to your navigation. If you continue to browse, we consider you accept this use. See more information on our cookies policy here.

Annual Report 2012

- Corporate Social Responsibility

- Independent Panel of Experts on Sustainability Development

- IPESD on the 2011 CSR Report

1. In view of Abengoa’s long term commitment to cleaner energy and to combating climate change could the company provide data on GHG emissions for several years and explain GHG trends (including intensity ratios)?

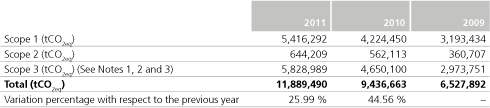

Beginning in 2008 and up to the present, three annual greenhouse gas (GHG) inventories have been published and externally verified for the years 2009, 2010 and 2011. Over the course of the past year, this verification was conducted in line with the specific requirements of Section 7.3 of the ISO 14064-1 Standard through a systematic, independent process documented by Aenor with a reasonable level of assurance.

The chart below shows a summary of Abengoa’s GHG emissions listed in all published inventories, as well as percentage variations with respect to the previous year.

GHG Emissions (tCO2eq)

Note 1: Scope 3 data shown in the table include emissions associated with work-related travel, work commutes, losses in the transmission of electrical power, emissions in the value chain of fuels consumed for generating acquired electrical power and supply-linked emissions.

Note 2: Data on work-related travel for 2010 (included under Scope 3) was modified with respect to the data published in CSRR2011 after detecting an irregularity in the consolidation process, quantified with an excess of 8,350 tCO2eq, equivalent to a variation of 0.09 % over the total figure for Abengoa’s GHG emissions in 2010.

Note 3: Data on supply emissions for 2011 (included under Scope 3) was modified following the detection of an error identified in the Abengoa Bioenergía Agroindustria Agrícola company, whose supply-related emissions as of the close of the 2011 inventory totaled 1,809,813 tCO2eq, for a total figure of 674,093 tCO2eq upon rectification of the error.

In absolute terms, CO2 emissions have been increasing over time, but in order to contextualize this rise, the following must be taken into account:

As a result of the natural maturity process of the GHG emissions management system, through optimization of emissions accounting and periodic review on all organizational levels, the group companies have been improving the quality of their emissions reporting year after year to reach the current level of maturity.

Furthermore, carrying out accurate global emissions accounting requires analysis of the variation in activity within the organization, which is a factor with a significant distorting effect on results. Thus, a company that has experienced more activity during a year than in the preceding year will also necessarily see an increase in its emissions. Success in lowering GHGs therefore lies in achieving an emissions increase that is lower than the rise in activity.

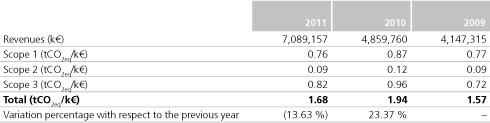

Given the heterogeneity of Abengoa’s activities and a lack of common aspects among them, in order to eliminate this distorting effect, the “revenues” parameter, the only common activity parameter, was used to perform the calculation by means of the following formula:

Provided below is a table showing the emissions/revenues ratio for the three annual inventories published to date:

Emissions intensity with respect to revenues

As we can see, Abengoa reduced the intensity of its carbon emissions in 2011 by 13.63 %, a figure obtained in global terms. This abatement, in a scenario characterized by a high increase in company activity, as shown in the last table, was the result of designing and implementing emission reduction plans throughout the Abengoa companies.

Additionally, Abengoa has estimated global reductions achieved by conducting a comparative study between “GHG emission/activity parameter” ratios for one year and those from the preceding year in each one of the group’s companies. In calculating emission reduction, a reality-adjusted activity parameter (for example, revenues, production or number of hours worked) was selected for each company in order to contrast the parameter with its GHG emissions (See Notes 4 and 5).

- 2010 reductions over the 2009 annual inventory: 550,000 tCO2eq

- 2011 reductions over the 2010 annual inventory: 360,000 tCO2eq

Note 4: Emission reduction estimations are not intercomparable due to the fact that they are obtained through analysis which applies differing levels of exhaustiveness and activity parameters. For example, 2010 emissions reduction with respect to 2009 includes reductions from the Telvent business unit, which ceased to be a part of Abengoa in 2011.

Note 5: Emission reduction calculations were improved in 2011 with respect to those from the preceding year through the use of activity parameters that are more in line with Abengoa’s different business typologies. These parameters shall remain in place with a view to the future.

It should be pointed out that the calculation of emission reduction estimations was obtained through a company-level study, whereas emission intensity estimations (previous table) were computed globally.

2. Can Abengoa describe its approach to the biodiversity, water and human health impacts of its major infrastructure construction contracts and the specific measures taken to mitigate these impacts?

Committed to the sustainability of its products and processes, Abengoa is a company that dedicates its efforts to developing technological solutions aimed at securing sustainability development and towards making sure that the process of developing these solutions is itself sustainable. As far as biodiversity, water, and human health are concerned, the organization promotes measures to ensure biodiversity protection, reduce water consumption, and lower any negative impacts which company activity may have on people’s health.

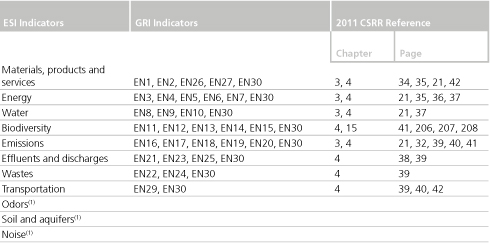

To monitor these aspects, Abengoa devised the Environmental Sustainability Indicators (ESI)6 that aid in determining company impact through the analysis of eleven factors (water, biodiversity, noise, odors, transportation, emissions, effluent discharges, raw materials, soil and aquifers, and waste) and setting targets for improvement.

In addition to the abovementioned indicator procedure, Abengoa applies specific measures to manage the impact of company activity on the environment. In relation to biodiversity, such initiatives involved an investment of 5 M€ in 2012, and primarily consisted of: restoring affected areas, lowering pressure on remaining natural forests (native forests), and biodiversity conservation, including monitoring of plant and animal species composition. Archeological and paleontological studies are also conducted to determine whether a project affects any fossil or archeological sites.

The company’s commitment to sustainability is furthermore manifested in the obligatory nature of environmental management system certification for all group companies with activity in accordance with the international ISO 14001 standard.

These norms are extended to include all infrastructure construction contracts and require identification of and compliance with prevailing laws and regulations that apply to each project. In the case of construction of more significant infrastructure, it is necessary to conduct specific studies on environmental and social impact; determine, evaluate and monitor significant environmental aspects associated with project activities; and develop and implement operational control mechanisms applied to construction work in order to make sure that activities which may potentially lead to environmental or social impacts are managed accordingly.

In addition, emergency plans are developed and implemented through environmental simulation drills, and all employees are trained in areas related to environmental protection, which generates cross-cutting environmental awareness that in turn gives rise to a proactive approach to environmental conservation.

One example of what we have described above is the loan agreement signed in 2011 with the Inter-American Development Bank for financing infrastructure construction projects in Latin America. This document establishes highly stringent requirements involving sound environmental and social practices that must be abided by before, during and after project execution; and also includes audits and checks to be conducted by this institution in order to verify compliance.

(1) Data related to these indicators is not yet available to Abengoa; however, Abengoa has conveyed the importance of measuring impact in relation to these factors throughout the group companies.

Social development area

3. Can Abengoa explain the methods and the sources of data used to make the economic analysis of its contribution to society (local economic development, locally sourced purchasing, local business and community development) - see references to Economic Value Distributed and in the Community section of the Report?

Abengoa performs economic analysis of the company’s contribution to society in accordance with the indicators outlined in Global Reporting Initiative (GRI) Guide 3.1. Specifically, the question refers to six indicators which Abengoa reports as follows:

- EC1: Taxes paid; the total amount of taxes paid is reported separately for the countries that add up to at least 95% of the total amount of taxes paid in absolute numbers.

- EC1_SO1: Actual or anticipated external social engagement undertaken during the reporting period to benefit society.

- EC1_EC4: Value creation and financial assistance received from governments.

- EC6: Policy, practices, and proportion of spending on locally-based suppliers at significant locations of operation.

- EC8: Development and impact of infrastructure investments and services provided primarily for public benefit through commercial, in-kind or pro-bono engagement.

- SO9_SO10: Operations with potential or actual negative impacts on local communities, and prevention and mitigation measures implemented in operations with potential or actual negative impacts on local communities.

These performance indicators, along with the other GRI Guide indicators, are captured and reported through the Integrated Sustainability Management System (ISMS). The primary objective of this system is to gather objective, consolidated data pertaining to sustainability in order to measure and compare the impact of company activities, set targets for improvement and report them in a transparent manner.

The scope of the information contained in the system, which, in the case of the indicators described, involves quarterly or half-yearly reporting, refers to all companies that are under the operational management or control of Abengoa.

The data are compiled and entered into the system from the company work locations, and are verified and consolidated at different levels (company and business unit). In addition, for every indicator there is an individual in charge of consolidating the data for the entire organization and performing final validation.

Data reported through the system are verified annually by an independent external entity. In 2011, auditing was conducted by PwC.

Among the initiatives through which Abengoa contributes to the development of the communities where the company operates is the PE&C social development program: People, Education and Communities: Committed to Development.

Since its inception in 2005, PE&C has helped around 8,000 people in the countries where the program has been implemented: Argentina, Peru, Brazil, Mexico, India, and Chile.

Through education and training, PE&C pursues social development and integration of the most vulnerable social groups: children, women, the disabled, and the elderly, providing them with tools aimed at empowering them to ensure themselves a sustainable future.

Along these lines, another specific initiative carried out by Abengoa to foster community economic and social development is the transmission line technician school in Peru. Through this program, the company seeks to attract and train people without experience in high-voltage tower assembly for subsequent incorporation as members of the company staff, where they can put what they have learned into practice.

4. Can Abengoa report on the enforcement of commitments from suppliers under the Social Responsibility Code and GHG emissions reporting agreements and what plans exist to achieve greater audit coverage of suppliers rated as high risk?

True to its commitment to transparency and the ability to convey sustainability-related values and principles to the supply chain, Abengoa publishes data on the CSR agreements signed with company providers in the annual Corporate Social Responsibility Report:

- Number of suppliers and subcontractors who have signed up to the Social Responsibility Code (SRC), which contains 11 clauses based on the principles of the United Nations Global Compact and inspired by the international SA 8000 standard. Through this agreement, providers undertake a commitment to fulfill all aspects involving social and environmental responsibility included under the agreement and agree to potential inspections of their facilities.

- Number of Greenhouse Gas Emissions Reporting System Implementation agreements, through which suppliers have an obligation to provide Abengoa with the information on the emissions associated with each product or service contracted. Emissions data submitted by suppliers are integrated into the Integrated Sustainability Management System (ISMS) and consolidated in Abengoa’s annual greenhouse gas emissions inventory.

To monitor compliance with both agreements, Abengoa has a variety of tools which help to ensure that suppliers abide by the terms of the clauses and to convey company values to the supply chain, thereby warding off any actions which might contravene our principles of conduct. The primary mechanism is supplier auditing. Supplier-related risk analysis is conducted annually, focusing on location and nature of activity, among other parameters. Our suppliers are audited based on this analysis and the level of risk and criticality identified. Audits may be performed on a remote basis, using self-evaluation questionnaires or by submitting documentation, or in person, as in the case of audits conducted at the supplier’s own facilities.

Along these lines, in 2011 Abengoa set out to develop a Responsible Procurement System that incorporates sustainability criteria into supplier assessment. The ultimate aim of this system, which includes the aforementioned audits, is to establish a supplier ranking according to sustainability levels.

As its minimum target, Abengoa has established that onsite audits be carried out for 5 % of the suppliers determined to be high-risk. Fifty-five (55) audits of this type were conducted in 2011 alone, which represents 9 % of the critical suppliers identified.

Since the system was implemented, Abengoa has made headway in identifying critical suppliers with the aim of ensuring compliance with our principles of conduct throughout the supply chain.

In addition to the supplier audits, Abengoa engages in other monitoring activities intended to ensure compliance with the agreements signed by the company’s providers, including internal audits and monitoring and follow-up visits, which take place annually in Abengoa companies and involve, among other aspects, verification of proper functioning of the systems that make up the ISMS: the GHG inventory, where supplier emissions are computed; and the CSR indicator system, which records the number of signed agreements, the number of locally-based suppliers, etc.

During the supplier audits conducted in 2012 a number of cases of non-conformity were found related to incidents involving installation operating licenses; deficiencies in payments to the social security or guarantee fund; overtime exceeding legal limits; as well as some incidents involving fulfillment of legal requirements associated with health and safety: the absence of a physician in the workplace, failure to conduct a first aid course, absence of a medical checkup program or the lack of an environmental risk prevention program.

Whenever a case of “non-conformity” is detected, Abengoa draws up an action plan which results in a collaborative effort undertaken with the supplier so that the latter may adapt to the established requirements. The aim of working with these providers is to resolve situations of non-compliance, with a view to transmitting responsible conduct to our supply chain.

There nevertheless exists the possibility of ceasing to work with a provider that has fallen into “non-conformity” if the supplier fails to rectify the incidents detected. In this regard, in 2012 Abengoa stopped working with five suppliers who exhibited failure to comply with standards pertaining to sustainability management.

5. What processes does Abengoa seek to put into practice for implementing the principles of the Ruggie guide to human rights?

In accordance with the principles governing the Ruggie Framework, Abengoa works towards preventing its activities from bringing about or contributing to bringing about negative consequences for human rights, while at the same time endeavoring to prevent or mitigate negative effects on human rights that are directly related to the operations, products or services provided by its commercial relations, even when the company has not contributed to generating such effects.

The initiatives Abengoa carries out to uphold the Ruggie principles are realized through specific actions linked to fulfillment of company objectives. Noteworthy among them are the following:

- Holding at least ten Labor-Related Social Responsibility (LSR) meetings per year.

- Monitoring and follow-up of all processes needed for satisfactory incorporation of new members into the company workforce.

- Establishing control mechanisms to prevent failure to uphold the ban on the use of child labor and forced labor.

- Verification of SA8000 Standard compliance through two annual audits.

- Monitoring of the degree of implementation of LSR policy across Abengoa companies.

- Measurement and monitoring of the LSR indicators.

- Corroboration to the effect that 100 % of suppliers are informed regarding company CSR policy through a signed commitment.

- Verification to the effect that all new company employees are informed regarding the potential risks of their job positions.

- Evaluation and communication of work climate survey results. This survey is conducted every two years among company employees, and improvement actions are implemented based on survey results.

- Analysis of personnel turnover rate with respect to the previous year.

- Supervision of compliance with legal requirements and other agreements signed by the organization.

Abengoa expresses its commitment to human rights through a policy statement which, in our case, is based on our company’s Code of Conduct.

The Abengoa Code of Conduct sets forth measures aimed at preventing the occurrence of incidents relating to the infringement of human rights, and lists corporate values, in conjunction with the requirement of adhering to the highest standards of honesty and ethical conduct, including procedures for dealing with conflicts involving personal and professional interests. The code also calls for the utmost confidentiality and fair treatment inside and outside Abengoa, and requires immediate internal communication of code violations and any kind of illegal conduct. In the event that an incident is reported, the strictest confidentiality surrounding the whistleblower and the case is maintained at all times.

In addition to the internal whistleblower channel, all stakeholders have access to an external whistleblower channel for reporting any company-related practices that contravene the principles and values set forth in the organization’s Code of Conduct.

Both channels are managed by the auditing committee of the different group companies, and this body is in charge of safeguarding such confidential information.

This protection of basic rights is in turn extended to include the supply chain through mandatory signing of the Social Responsibility Code (SRC), which specifies company policy regarding protection of human rights, prior to engaging in any activity with the organization. In order to ensure fulfillment of this code, the company performs supplier audits where providers are categorized as being high-risk following preliminary analysis.

Furthermore, as a signatory to the United Nations Global Compact, Abengoa works towards integrating into its strategy the ten principles revolving around protection of human rights, environmental conservation and anti-corruption, and reports on this process on an annual basis.

6. How does the company assure itself that it reaches all employees and subsidiaries with its range of sustainability commitments, targets and processes, taking into account the wide variety of legal and cultural environments across the countries where Abengoa operates, and how is the effectiveness of these outreach efforts measured?

The main instrument Abengoa utilizes to ensure that company strategy is deployed uniformly at all levels and in all geographical locations of company operation consists of the Common Management Systems, which constitute the internal method for evaluating and controlling risks and represent a common culture in managing Abengoa’s businesses based on sharing knowledge accumulated and establishing performance guidelines and criteria.

The risk management model in place at Abengoa is executed via three components: NOC (Norms of Obligatory Compliance), POC (Processes of Obligatory Compliance), and the URM (Universal Risk Model).

The NOC and POC are common throughout the company and are continually updated in order to adapt them to the reality of the organization.

The NOC feature an internal system of authorizations and communications in constant evolution so as to enable them to mitigate risks associated with company activity. The company’s commitments, processes and objectives are incorporated into these norms which are updated, reviewed and communicated to all employees on an ongoing basis. Mandatory (attendance-based and on-line) annual courses are also conducted to reinforce employee knowledge of these internal standards.

A total of 25,035 attendance-based hours and 27,780 online hours were dedicated to NOC training instruction in 2011.

The Procedures of Obligatory Compliance help lower company risks through a combined system of control procedures and activities in key areas.

Finally, the URM ensures identification, understanding and assessment of risks that affect Abengoa by devising an efficient response system in line with the company’s business objectives. Risks are monitored through a series of probability indicators according to the nature of each risk.

Proper URM compliance is ensured through approval flows in the data entry and updating processes, in addition to committee meetings held on a regular basis by the Chairmanship and General Management.

With regard to all of the above, Abengoa conveys the organization’s sustainability engagement to its employees through training courses aimed at minimizing environmental impacts and training on sustainability development and combating climate change. In addition, communications are issued continually on the initiatives being implemented by the organization as part of its commitment to sustainability.

In 2011, 30,853 hours of instruction were dedicated to this area.

7. Customer satisfaction surveys are conducted but the message to readers of the Report remains unclear. Did these show improving levels of satisfaction or the reverse? What actions is Abengoa taking in response to these results?

Due to the diversity of Abengoa’s businesses and the wide-ranging, particular features of its products and customers, at present there is no centralized, homogeneous system in place to measure overall satisfaction. Whether due to being an ISO 9001 requirement or as the result of applying sound management practice-related criteria, practically all Abengoa companies carry out their own studies, establishing improvement plans and objectives in response to the analysis of the measurements taken.

Following completion of each project, Abengoa sends out a satisfaction questionnaire to its customers. The questionnaire evaluates the project globally, from the offering to the delivery of final documentation. In order to manage these questionnaires and the analysis of the communications received from customers, a computer application referred to as the External Evaluation Process (EEP) has been implemented.

The quality and environment committees are in charge of evaluating the results of the evaluation surveys. In the event that values falling below the control level established for each year are detected, these committees determine the measures to be implemented according to the needs identified.

Improvements were made to the EEP questionnaire in 2010 through the inclusion of consultations which enable assessment of the activity to be conducted in comparison with the competition, and the addition of a question regarding overall satisfaction, with this information enabling the company to weigh the importance the customer attaches to each one of the aspects taken into consideration in the survey.

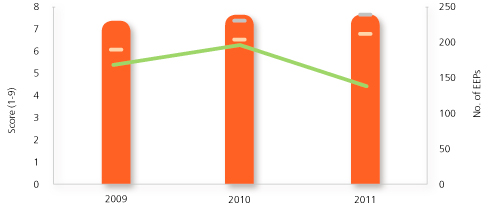

Provided below as an example is the customer satisfaction analysis for Inabensa, an Abengoa company with an order volume totaling over 500 M€ in 2011.

Note 1: Control Level, this refers to the minimum acceptable value in the level of customer satisfaction. In the event that this value is not exceeded, the result would be analyzed during the Quality and Environment Committee meeting sessions in order to make appropriate decisions aimed at improving the result.

Note 2: Target, the desired value of attainment for improving satisfaction results based on an improvement plan. Example: “Target set in 2010: to improve the degree of customer satisfaction by achieving an increase of at least 2 tenths of a point in the overall assessment of the ‘Offering Quality’ and ‘Final Documentation’ attributes”. Improvement plan implementation and efficiency is verified during the Quality and the Environment Committee meetings and through the systems review conducted by management on an annual basis.

Additionally, with a view to presenting aggregated information to globally represent Abengoa customer satisfaction, regardless of customer typology, an indicator was incorporated into the Integrated Sustainability Management System (ISMS) in 2012 for the purpose of compiling the satisfaction survey results that will be published in this report.

8. How has the company responded to improve performance in the realm of Health, Safety and the Environment with respect to accidents resulting in fatalities?

Any Work-related Accident (WA) occurring at Abengoa is analyzed in depth to determine causes and establish the measures needed to prevent reoccurrence. Along these lines, monitoring of all initiatives and measures adopted is conducted through the Occupational Risk Prevention (ORP) Committees that have been set up at all companies with high accident risks and in all companies with 50 or more workers.

In order to address any investigation process involving work-related accidents, Work-related Diseases (WD), adoption of measures aimed at prevention and protection, governmental or customer intervention, etc, Abengoa companies are required to implement a TSR (Troubleshooting computer tool) or an IA (Improvement Action Tool) to facilitate participation by the affected organization and the ORP service in solving problems and proposing initiatives aimed at improvement. Evolution and closure of the TSR/IAs is evaluated during company ORP committee meetings.

In accordance with the OHSAS18001 Standard, Abengoa companies that are certified under this norm set Occupational Risk Prevention targets in line with the analyses performed by management and with the needs ascertained through this analysis. Proposal and approval of these targets takes at the company’s ORP Committee Meeting, and they are subsequently approved by General Management, and the same body carries out periodic monitoring of evolution and fulfillment of the objectives established.

Whenever serious accidents or accidents resulting in fatalities occur, involving both the company’s own personnel as well as contractors, the method employed to manage these situations is similar.

- The top priority is attending to the accident victim as quickly as possible and reporting on what has occurred to his or her family.

- Internal communication regarding the accident throughout the organization and at all hierarchy levels in accordance with internal procedures and regulations.

- External communication regarding the accident (customers, labor-related administration, etc.).

- In-depth investigation of the accident that has occurred.

- Issuance of the corresponding investigation reporting including a description of the incident and prevention and protection measures proposed for adoption.

- Implementation of the corresponding Troubleshooting Report (TSR), an internal tool which makes the analysis of a specific problem and the solution proffered available throughout the organization.

- Implementation of the measures drawn up for application (training, provision of human and material resources, working procedures, etc.).

- Monitoring and follow-up on steps taken through the company prevention committees.

- Where applicable, proposal of good practices applied in other organizations dedicated to similar activities.

- And, in parallel, study and analysis of each case, with Abengoa’s Corporate ORP Committee establishing the opportune improvements.

9. Given the large family ownership of Abengoa, can the company give an analysis of shareholdings by location and size?

As of the end of the first half of the year, Abengoa’s free float1 stood at 43.96 %. Free-float capital is that which is not controlled by either the Board or by senior management, nor is it part of the treasury stock.

One of the functions of the investor relations team is to identify and monitor all of Abengoa’s shareholders. Coinciding with the quarterly closings of earnings results, four analyses of Abengoa’s free-float capital structure and composition are conducted throughout the year. This exercise enables the organization to determine and track the company’s shareholder composition and evolution. All shareholders are categorized according to size, position, most recent transactions, geographical location, and their last capital position.

As of the end of the first half of the year, date upon which the latest analysis was conducted, we know that 45 % of Abengoa’s free-float capital is in the hands of institutional shareholders. Shareholder identification is carried out based on their investment methods and return expectations, as well as geography and investment time horizon.

Comment for the IPESD: for reasons of confidentiality, Abengoa does not publish information related to the breakdown of its shareholders. As far as the company’s controlling stakeholder (Inversión Corporativa) is concerned, information pertaining to composition is public and available through the Mercantile Registry (MR) of Spain.

Does Abengoa have a process for the selection of members of the Board of Diretors that ensures that minority shareholders can be represented in strategic decision making and on other issues affecting their rights?

The independent director plays a significant role on the listed company’s Board of Directors in protecting the company’s general interest, and, in turn, safeguarding the interests of minority groups. Abengoa, aware of the important task performed by the independent director, applies a rigorous method for selecting independent directors.

The Appointments and Remuneration Committee is the body which is in charge of selecting from among professionals of recognized national and international prestige in different areas whose backgrounds best represent the needs of minority shareholders. The selection procedure is based on merit and professional profile, not on particular interests. It also verifies on an annual basis that the conditions of convergence in designating directors and the nature or typology assigned to them are upheld. The Appointments Committee likewise ensures that selection procedures do not hinder the selection of female directors and promotes the inclusion of women with the desired background from among potential candidates. The committee also reports to the Board of Directors on Board nominations, reelections, resignations and remuneration of the Board and its directors, and regarding the general policy on remuneration and incentives for board members and senior management. Furthermore, the committee informs on all proposals which the Board of Directors takes up at the General Meeting regarding appointment or termination of directors, even in the event of co-opting by the Board of Directors itself.

In addition, an Independent Verification Review of the Annual Report on Corporate Governance of Abengoa, S. A. is prepared each year by external auditors to ensure that report contents are in line with both the recommendations established in the Special Working Group Report on good governance of listed companies (Unified Good Governance Code), as well as the modifications introduced by Law 2/2011 on Sustainable Economy dated March 4th. A level of reasonable assurance, which is the highest possible level of assurance, was obtained in 2011 in the review performed by PricewaterhouseCoopers Auditores, S. L.

All of the above is reinforced by the International Advisory Board, whose efforts dedicated to providing guidance in strategic matters contribute towards greater understanding by Abengoa of the needs of its different stakeholders, with its main interlocutor being the independent director.

10. The discussion of materiality definitions for CSR reporting purposes does not make clear how stakeholders, especially external ones, are identified for consultations, how many interviews were conducted and how their input was weighted. Can Abengoa supply this information?

In 2011, Abengoa carried out a detailed study of materiality on the basis of two perspectives in analysis: external and internal.

Through this analysis, expectations were identified, as well as the issues determined to be material for the company’s stakeholders (customers, suppliers, shareholders, employees, communities and society) in order to ascertain the issues affecting and of concern or interest for each stakeholder and attempt to address these matters appropriately.

In analyzing materiality from an external perspective, the following were examined:

- Requirements of international reporting standards such as the Global Reporting Initiative (GRI) and the AA1000 AS (2008).

- Best practices in CSR of industry companies and those recognized by the market as leaders in sustainability.

- Main issues taken into consideration in sustainability indexes like the Dow Jones Sustainability Index (DJSI) or the FTSE4Good.

- Commitments undertaken by the company through adherence to international initiatives that include Caring for Climate and the United Nations Global Compact.

- Reader opinions on reports from previous years taken in through the variety of communication channels provided by the company.

- Presence in national and international media, facilitating the interpretation of the materiality of public opinion.

- Public information from associations and institutions linked to the energy and environment sectors that are working in areas of interest for Abengoa.

In order to determine issues relevant for the company from an internal perspective, specific committees made up of employees from the company’s different business divisions and working areas were set up. Through a secret voting process carried out during committee meetings, a series of issues related to corporate values, policies, strategies and staff concerns was obtained.

A prioritized list of issues deemed to be material for the company and its stakeholders was drawn up upon completion of the two analyses.

With a view to reinforcing the materiality of the issues identified as being of relevance, the members of the different internal committees, which met to carry out the Relevant Matter Procedure (RMP), came up with a representative sample of all Abengoa stakeholder typologies (customers, suppliers, employees, shareholders, investors, society, and communities) that were interviewed to gather information related to the expectations of the range of stakeholders. A total of 24 individual interviews were conducted to thoroughly analyze different aspects that include: promoting diversity, non-discrimination, development of practices and policies aimed at fomenting labor stability, the inclusion of ESG risks in risk management, definition of a specific climate change policy or strategy, as well as, among others, determining and assessing the CO2 footprint. The issues analyzed were included in the study of materiality representing stakeholder expectations.

In order to ensure the objectivity of the procedure, the interviews were conducted by an outside consultant, and the utmost confidentiality of the responses was upheld so that, except where the interviewee expressed a desire to the contrary, the identity of the stakeholder representatives went on to become anonymous.

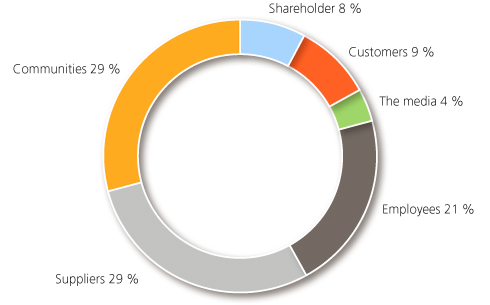

Distribution of stakeholders analyzed

For the third consecutive year, in 2011 Abengoa obtained reasonable assurance in the application of the three principles of the AA 1000AS (2008) Standard: inclusivity, relevance, and responsiveness, which constitute the framework for the company’s relationship with its stakeholders.

Customer Satisfaction – Overall Assessment

© 2012 Abengoa. All rights reserved