Annual Report 2010

- Legal and Financial Report

- 2010 Consolidated Annual Accounts

- Notes to the Consolidated Financial Statements

-

Note 1.- General Information and Business Overview

1.1. General information

Abengoa, S.A. is the parent company of the Abengoa Group (referred to hereinafter as “Abengoa”, “the Group” or “the Company”), which at the end of 2010, was made up of 645 companies: the parent company itself, 595 subsidiaries, 21 associates and 28 joint ventures. Additionally, as of the end of 2010,certain group companies were participating in 353 temporary joint ventures (UTE) and, furthermore, the Group held a number of interests, of less than 20%, in several other entities.

Abengoa, S.A. was incorporated in Seville, Spain on January 4, 1941 as a Limited Partnership and was subsequently changed to a Limited Corporation (“S.A” in Spain) on March 20, 1952. Its registered office was at Avenida de la Buhaira, 2, Seville (Spain). On January 25, 2010, the Board of Directors agreed to move the registered office to Campus Palmas Altas, plot ZE-3, 41012 Seville, amending Article 2 of the Bylaws accordingly and recording the new address in the Companies Register.

The Group’s corporate purpose is set out in Article 3 of the Articles of Association. It covers a wide range of activities, although Abengoa is principally an applied engineering and equipment manufacturer, providing integrated project solutions to customers in the following sectors: Engineering, Telecommunications, Transport, Water Utilities, Environmental, Industrial and Service.

Abengoa’s shares have been listed in the Madrid and Barcelona Stock Exchanges since November 29, 1996 and are currently included in the Ibex-35, the selective index for Spanish listed entities.

These financial statements were approved by the Board of Directors on February 23, 2011.

It is possible to view all public information regarding Abengoa on the Group’s website at www.abengoa.com.

1.2. Business overview

Abengoa is an international company that applies innovative technical solutions for the sustainable development, primarily in the environment and energy sectors, obtaining energy from the sun, producing biofuels, desalinating sea water or recycling industrial waste.

Abengoa’s head office is in Seville (Spain) and the company is present, with its subsidiaries and other companies, in which it holds shares, as well as with installations and offices, in over 70 countries, operating through the following five business groups, which constitute the operating segments to which IFRS 8 refers:

1. Solar

Abengoa Solar is the holding company of this business unit. Its activity is focused on the development and application of solar energy technologies in the fight against climate change, in order to ensure sustainable development through its own solar thermal and photovoltaic technologies.

2. Bioenergy

With Abengoa Bioenergía as its holding company, this business unit is engaged in the production and supply of biofuels for transport (bioethanol and biodiesel amongst other products) which use biomass (cereals, cellulosic biomass, oleaginous seeds) as a raw material. Biofuels are used in the production of ETBE (a gasoline additive) or can be mixed directly with gasoline or diesel. As a renewable energy source, biofuels reduce CO2 emissions and contribute to the diversification and the guarantee of ongoing energy supply, reducing levels of dependence upon traditional fossil fuels as a source of energy as well as collaborating and complying with the Kyoto Protocol.

3. Environmental Services

With Befesa Medio Ambiente as the holding company, the group is an international business unit specializing in the integrated management of industrial waste as well as the management and generation of water, which is a key social responsibility for the creation of a sustainable world.

4. Information Technologies

The parent company of this business unit is Telvent GIT, S.A. and it is the service and Information Technologies company engaged in working for a safe and sustainable world through the development of high-value-added integrated systems and solutions in Energy, Transport, Agriculture, the Environment, Public Administrations and Global Services.

5. Industrial Engineering and Construction

With Abeinsa as its parent company, the industrial and technology business group offers integrated solutions in the energy, transport, telecommunications, industry, services and environmental sectors. These innovative solutions, geared towards sustainability, enable value creation for the customers, shareholders and employees, ensuring a profitable future with an international dimension for its investors.

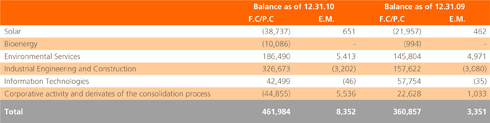

Although extensive information on the five reporting segments of Abengoa is given in Note 40, consistently with the financial information which has been reported to the Chief Operating Decision Maker (see Note 2.28) up to the end of the current fiscal year, it is important to point out that due to the effort of continuous evolution and transformation that Abengoa has been incurring for over more than 15 years, Abengoa’s management started to utilize information by business activity and to present, in addition, financial information based on three single business activities that best represent, in management’s view, Abengoa’s current business environment. During 2011, it is expected that such financial information based on the three business activities will represent the discrete financial information which will be reviewed by the Chief Operating Decision Maker to make decisions about the allocation of resources to those business activities and to assess their performance.

In relation to the above, it should be noted that Abengoa, international technology company, focuses on two sectors, energy and environmental, and three business activities, that are Engineering and Construction, Concession-type Infrastructures and Industrial Production.

Therefore, the business activities of Abengoa and its management and internal financial information, will be structured, starting from 2011, based on the following business activities:

- Engineering and Construction: it relates to the business activity which incorporates all of our traditional activity in engineering, water and information technologies, with over 70 years of experience in the market and where we are specialists in the execution of complex turn-key projects of thermosolar plants, hybrid gas-solar plants, hydraulic infrastructures including complex desalination plants, biofuel plants, electrical transmission lines, and critical control systems for infrastructures, among others. Additionally, the Group is the leader in information and services technology in critical sectors.

- Concession-type Infrastructures: it relates to the business activity that groups together the activity of operating assets associated to a long term sale contract, such as “take or pay”, tariff or “power purchase agreement”. These are assets related to solar power plants, transmission lines, cogeneration plants and desalination plants for which we have a low risk of demand and our efforts are focused on its optimal operation.

- Industrial Production: it relates to the business activity that groups Abengoa’s biofuel activity and recycling of industrial waste and salt slag. These activities, are carried out through Group’s own assets and are focused in high growth markets in which the company holds a leadership position.

In connection with the above, although the segment information presented in note 40 includes financial information based on the five Abengoa’s traditional business segments, in order to facilitate the comprehension of the financial information, during this period which has been considered as transitory, management considered useful to present additional financial information for the three business activities mentioned above.

-

Note 2.- Significant Accounting Policies

The significant accounting policies adopted in the preparation of Abengoa’s Consolidated Financial Statements are set forth below:

2.1. Basis of presentation

The Consolidated Financial Statements for the year ended December 31, 2010 have been prepared in accordance with International Financial Reporting Standards, as adopted for use within the European Union (herein, IFRS-EU).

Unless stated otherwise, the accounting policies as set forth below have been applied consistently throughout all periods shown within these Consolidated Financial Statements.

The Consolidated Financial Statements have been prepared under the historical cost convention, as modified by the revaluation of available-for-sale financial assets, and financial assets and financial liabilities (including derivative instruments) at fair value through profit or loss.

The preparation of the Consolidated Financial Statements under IFRS-EU requires the use of certain critical accounting estimates. It also requires that Management exercises its judgment in the process of applying Abengoa’s accounting policies. Note 3 provides further information on those areas which involved a greater degree of judgment or areas of complexity for which the assumptions or estimates made are significant to the financial statements.

The figures included within the components of the Consolidated Financial Statements (Statement of Financial Position, Income Statement, Statement of Comprehensive Income, Statement of Changes in Equity, Cash Flow Statement and these notes herein) are, unless stated to the contrary, all expressed in thousands of Euros (€).

Unless stated otherwise, any percentage shareholdings shown include both direct and indirect ownership.

The IASB recently approved and published certain Accounting Standards amending the existing standards, as well as IFRIC interpretations, from which the Group adopted the following measures:

a) Standards, interpretations and amendments thereto effective from January 1, 2010 applied by the Group:

- IFRS 3 (revised), ‘Business combinations’, and consequential amendments to IAS 27, ‘Consolidated and separate financial statements’, IAS 28, ‘Investments in associates’, and IAS 31, ‘Interests in joint ventures’, are effective prospectively to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after July 1, 2009.

The revised standard continues to apply the acquisition method to business combinations but with some significant changes compared with the previous version of the IFRS 3. For example, all consideration paid to purchase a business is recorded at fair value at the acquisition date, with contingent consideration classified as debt and subsequently remeasured through the income statement. There is a choice on an acquisition-by-acquisition basis to measure the non-controlling interest in the acquiree either at fair value or at the non-controlling interest’s proportionate share of the acquiree’s net assets. All acquisition-related costs are expensed. The Group has applied this Standard prospectively to business combinations from January 1, 2010 with no significant impact.

- IAS 27 (revised), “Consolidated and Separate Financial Statements”. The revised standard requires that the effects of all transactions with non-controlling interests be accounted for in the equity if no change of control occurs, meaning that these transactions cease to give rise to goodwill or profit and/or loss. The standard also establishes an accounting procedure applicable in the event control is lost. Any remaining interest held in the company must be remeasured at its fair value, and a profit or loss recorded in the income statement. The Group has applied this Standard prospectively to transactions with non-controlling interests as from January 1, 2010 with no significant impact.

- Amendment to IAS 39 “Eligible Hedged Items” (compulsory for all financial years starting from July 1, 2009 and its application is retroactive). This amendment introduces two major changes by prohibiting the designation of inflation as a hedged item in a fixed-rate debt, and prohibiting the designation of the time value in the hedged risk when options are designated as hedges.

As mentioned in Note 9, the risk management policies of interest rate hedging are based on the purchase of options in exchange of a premium (call option purchase) through which the company ensures paying a maximum fixed rate.

The application of this standard represents a change in the designation of the hedging instrument, as a result no change in the valuation of financial instrument takes place.

The group has applied IAS 39 (amended) with no significant effect on the consolidated financial statements.

- Amendment to IFRS 2, “Group Cash-settled Share-based Payment Transactions". This amendment clarifies the basis to determine the classification of share-based payment transactions in consolidated and standalone financial statements. The amendment includes in IFRS 2 the provisions previously included in IFRIC 8, “Scope of the IFRS 2” and in IFRIC 11, “IFRS 2 – Transactions with own shares and with those of the group”. The amendment also extends the IFRIC 11 guidance for agreements between companies within the same group which were not covered by this interpretation. The amended IFRS 2 covers grants liquidated in cash by a group’s company that does not have a contract with the employees receiving the grant. The Group adopted the amendment to IFRS 2 prospectively from January 1, 2010, with no significant impact on the consolidated financial statements.

- IFRS 5 (amendment), ‘Non-current assets held for sale and discontinued operations’. This amendment, part of the annual improvements project of the IASB for the year 2008, clarifies that all the assets and liabilities of a subsidiary shall be classified as held for sale if the enitity looses control of the subsidiary due to a partial plan for its sale. If the conditions to be classified as discontinued operations are fullfiled, the disclosures related to the subsidiary shall be presented. Consequently, IFRS 1 was also amended due to the changes introduced in IFRS 5, which will be applied prospectively from the date of the transition to IFRS. The amendment did not have impact on the consolidated financial statements.

- IFRIC 12, “Service Concession Arrangements”. This interpretation affects public – private service concession arrangements where the grantor governs what services the operator must provide using the infrastructure , to whom and at what price and also controls any significant residual interest in the infrastructure at the end of the term of the arrangement. In accordance with this interpretation, the infrastructure used in the concession arrangement may be classified as a financial asset or an intangible asset, depending on the nature of the payment rights established under the contract.

EC Regulation 254/2009 (March 25) established that European listed entities would be required to apply IFRIC 12 no later than by the start of the first annual period started on or after March 29, 2009. The Group has therefore applied IFRIC 12 since January 1, 2010 retrospectively and has restated all comparative information in accordance with that interpretation.

IFRIC 12 allows the separate accounting for the construction activities and for the subsequent operation and maintenance of the infrastructure, identifying that such activities present a business nature significantly different from each other and consequently have different business risks and rewards that should be recognised and measured separately.

Therefore the construction phase of the infrastructure should be recognised and measured using the applicable accounting method while the operation phase and the ordinary and extraordinary maintenance activities should be recognised and measured, for accounting purposes, in accordance with the contractual terms and the generation and the existence of the rights to the cash flows in favour of the operator for the services provided.

The application of such interpretation requires that certain specific requirements shall be met by the service concession arrangement, which normally includes the following two substantial aspects: a) the existence of an infrastructure that is controlled by the grantor; and b) the operation of the infrastructure implies rendering a public economic service in exchange for a price.

The retrospective application of IFRIC 12 did not have a significant impact on the consolidated annual accounts of Abengoa for 2010 as the company was already applying on a continous basis an accounting policy similar to IFRIC 12 for concession assets related to concessionary activities for electricity transmission, desalination and thermosolar generation.

The only impact derived from the application of IFRIC 12 consisted in a reclassification of concessionary assets under construction from the line Intangible Assets within the line item Fixed Assets in Projects (see the initial paragraph of Note 2.4 for the accounting treatment of Fixed assets of projects) amounting €679 and €389 thousand for periods ended December 31, 2009 and January 1, 2009, respectively.

Moreover, at the date of the first application of IFRIC 12, management carried out an analysis of the existing agreements within the Group and identified additional infrastructures that could potentially be classified as service concession arrangements, represented by certain thermosolar plants located in Spain, included in the pre-assignment register established under Royal Decree 661/2007 in November 2009.

In relation to this, management had initially concluded that, based on legal and technical reports from independent third parties, certain thermosolar plants met the requirements set out in IFRIC 12 to be considered as concession assets. Thus, the Group had recorded certain thermosolar plant as concessionary assets in the unaudited quarterly financial information presented to the Stock Market during the year 2010.

Notwithstanding the foregoing, Management has decided, in agreement with the regulatory body of the Spanish Stock Market, to further analyze and defer the application of IFRIC 12 to these thermosolar plants since, at the end of 2010, the arguments supporting this accounting application are not completely verified by the regulatory body, particularly as regards the public service nature of solar activity in Spain under the special regime of the Royal Decree 661/2007 and the register of pre-allocation.

- IFRIC 15, “Agreements for the Construction of Real Estate” (applicable for all financial years starting on January 1, 2010). This interpretation clarifies which transactirons must be accounted for in accordance with IAS 18, “Revenue” and IAS 11, “Construction Contracts”. The interpretation leads to the consequence of the likely application of IAS 18 to a larger number of transactions. This amendment did not have an impact on the Group’s financial statements.

- IFRIC 15, “Agreements for the Construction of Real Estate” (applicable for all financial years starting on January 1, 2010). This interpretation clarifies which transactirons must be accounted for in accordance with IAS 18, “Revenue” and IAS 11, “Construction Contracts”. The interpretation leads to the consequence of the likely application of IAS 18 to a larger number of transactions. This amendment did not have an impact on the Group’s financial statements.

- IFRIC 16, “Hedges of a Net Investment in a Foreign Operation” (applicable for all financial years starting on January 1, 2010). This interpretation clarifies the accounting treatment to be applied with respect to hedging of a net investment, including the fact that the net investment’s hedge refers to differences in the functional currency, not in the presentation currency, as well as that the hedging instrument can be held in any part of the group. The requirement of IAS 21 “The Effects of Changes in Foreign Exchange rates” is applicable to the item hedged. This amendment did not have a significant impact on the Group’s financial statements.

- IFRIC 17, ‘Distribution of non-cash assets to owners’ (effective on or after July 1, 2009).The interpretation was published in November 2008. This interpretation provides guidance on accounting for arrangements whereby an entity distributes non-cash assets to shareholders either as a distribution of reserves or as dividends. IFRS 5 has also been amended to require that assets are classified as held for distribution only when they are available for distribution in their present condition and the distribution is highly probable. This interpretation did not have impact on the consolidated financial statements.

- IFRIC 18, “Transfers of Assets from Customers” (effective for transfers received from July 1, 2009). This interpretation provides a guide on how to account for items of fixed assets received from clients, or cash received and then used to acquire or create some specific assets. This interpretation is only applicable to assets used to connect the client to a network or to provide it a continuous access or an offer of goods or services, or both. This interpretation did not have impact on the consolidated financial statements.

- Improvements to IFRSs published in April 2009 by the IASB, adopted by the EU in March 2010. The improvements published under the IASB’s annual improvement project are intended to deal with non-urgent and minor amendments to the existing standards. These improvements affect IFRS 2, 5 and 8; IAS 1, 7, 17, 18, 36, 38 y 39; and IFRIC 9 and 16. These improvements are mandatory as from January 1, 2010, except amendments to IFRS 2 and IAS 38 that apply to periods starting from July 1, 2009. These amendments did not have a significant impact on the Group’s financial statements.

As a result of the first time application of certain standards and interpretations that are applicable to the Group and that have been applied retrospectively from January 1, 2010, management has restated the applicable comparative figures of the consolidated annual accounts affected by such standards and interpretations.

Based on the above, and pursuant to IAS 1, "Presentation of Financial Statements” and IAS 8, "Accounting Policies, Changes in Accounting Estimates and Errors", the Group presents the Consolidated Statements of Financial Position for the comparative period (December 31, 2009) and the beginning of the earliest comparative period (January 1, 2009) with restated figures for comparability purpose.

b) New standards, amendments and interpretations issued but not yet effective and not early adopted

Revised IAS 24 (revised), ‘Related party disclosures’, issued in November 2009. It supersedes IAS 24, ‘Related party disclosures’, issued in 2003. IAS 24 (revised) is mandatory for periods beginning on or after January 1, 2011. The revised standard clarifies and simplifies the definition of a related party and removes the requirement for government-related entities to disclose details of all transactions with the government and other government-related entities. The group will apply the revised standard from January 1, 2011.

- ‘Classification of rights issues’ (amendment to IAS 32). The amendment applies to annual periods beginning on or after February 1, 2010. Earlier application is permitted. The amendment addresses the accounting for rights issues that are denominated in a currency other than the functional currency of the issuer. Provided certain conditions are met, such rights issues are now classified as equity regardless of the currency in which the exercise price is denominated. Previously, these issues had to be accounted for as derivative liabilities. The amendment applies retrospectively in accordance with IAS 8 ‘Accounting policies, changes in accounting estimates and errors’. The group will apply the amended standard from January 1, 2011.

- Amendments to IFRS 1, “Limited Exemption from Comparative IFRS 7 Disclosures for First-time Adopters”. This amendment is mandatory as from January 1, 2010.This amendment provides support for first-time adopters in the transition, as received when amendment in IFRS 7 “Financial Instruments: Disclosures” took place. That amendment required further disclosures of valuation at fair value and liquidity risk, and it was not mandatory to present comparative information. The group will apply the amended standard from January 1, 2011.

- ‘Prepayments of a minimum funding requirement’ (amendments to IFRIC 14). The amendments correct an unintended consequence of IFRIC 14, ‘IAS 19 – The limit on a defined benefit asset, minimum funding requirements and their interaction’. Without the amendments, entities are not permitted to recognise as an asset some voluntary prepayments for minimum funding contributions. This was not intended when IFRIC 14 was issued, and the amendments correct this. The amendments are effective for annual periods beginning January 1, 2011. Earlier application is permitted. The amendments should be applied retrospectively to the earliest comparative period presented. The group will apply these amendments for the financial reporting period commencing on January 1, 2011.

- IFRIC 19, ‘Extinguishing financial liabilities with equity instruments’, effective July 1, 2010. The interpretation clarifies the accounting by an entity when the terms of a financial liability are renegotiated and results in the entity issuing equity instruments to a creditor of the entity to extinguish all or part of the financial liability (debt for equity swap). It requires a gain or loss to be recognised in profit or loss, which is measured as the difference between the carrying amount of the financial liability and the fair value of the equity instruments issued. If the fair value of the equity instruments issued cannot be reliably measured, the equity instruments should be measured to reflect the fair value of the financial liability extinguished. The group will apply the interpretation from January 1, 2011, subject to endorsement by the EU.

c) Standards, amendments and interpretations to existing standards that have not been adopted by the European Union:

At the date this consolidated financial statements were being prepared, the IASB and IFRIC had published the standards, interpretations and amendments thereto, which are outlined below, whose effective date is January 1, 2010 or later dates:

- IFRS 9, “Financial Instruments”. This Standard will be effective as from January 1, 2013. This standard is the first step in the process to replace IAS 39, ‘Financial instruments: recognition and measurement’. IFRS 9 introduces new requirements for classifying and measuring financial assets and is likely to affect the Group’s accounting for its financial assets. The standard is not applicable until January 1, 2013 but is available for early adoption. IFRS 9 has not been endorsed by the EU, yet. The Group is currently assessing IFRS 9’s impact on the consolidated financial statements, in case of adoption by the European Union.

- IFRS 7 (modification) “Disclosures – Transfers of financial assets”(applicable for all financial years starting on July 1, 2011).

- Improvements to IFRSs published by the IASB: the improvements published under the IASB’s annual improvement project are intended to deal with non-urgent and minor amendments to the existing standards. These improvements are applicable as from January 1, 2011 and affect IFRS 1, 3 and 7, IAS 1, 27 and 34 as well as IFRIC 13.

- Deferred tax: Recovery of Underlying Assets (Amendment to IAS 12), effective from January.

2.2. Principles of consolidation

In order to provide information on a consistent basis, the same principles and standards as applied to the parent company have been applied to all other entities.

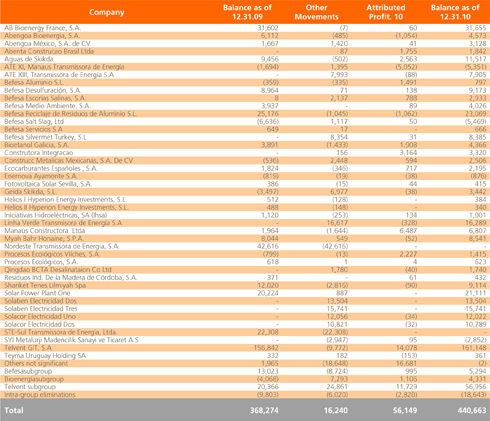

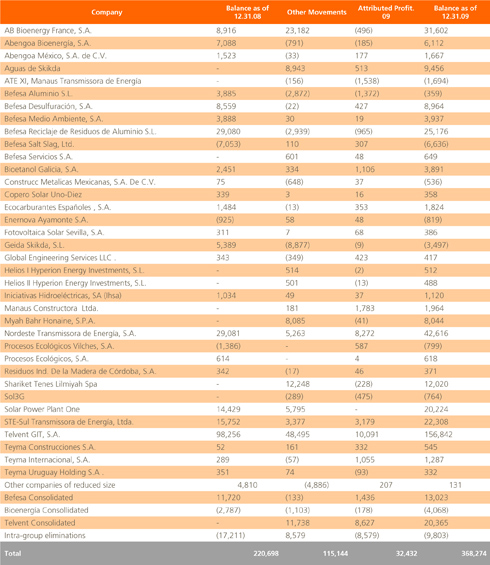

All subsidiaries, associates and joint ventures included in the consolidation for the years 2010 and 2009 that forms the basis of these Consolidated Financial Statements are set out in Appendixes I (VI), II (VII) and III (VIII), respectively.

a) Subsidiaries

Subsidiaries are those entities over which Abengoa has the power to govern financial and operational policies to obtain profits from their operations.

It is assumed that a company has control if, directly or indirectly (through other subsidiaries),it holds more than half of the voting rights of another company, except in exceptional circumstances in which it may be clearly demonstrated that such possession does not entail control.

Control shall also be said to exist if a company holds half or less of the voting rights of another and holds the following:

- power over more than half of the voting rights under an agreement with other investors;

- power to manage the financial and operating policies of the company, by virtue of a legal provision, a bylaw or some kind of agreement with the aim of obtaining profits from its operations;

- power to appoint or dismiss the majority of the members of the Board of Directors or equivalent governing body that is actually in control of the company; or

- power to cast the majority of the votes in meetings of the Board of Directors or equivalent governing body that controls the company.

Subsidiaries are accounted for on a fully consolidated basis as of the date upon which control was transferred to the Group, and are excluded from the consolidation as of the date upon which control ceases to exist.

The group uses the acquisition method to account for business combinations. The consideration transferred for the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred and the equity interests issued by the group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Acquisition-related costs are expensed as incurred. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. On an acquisition-by-acquisition basis, the group recognises any non-controlling interest in the acquiree either at fair value or at the non-controlling interest’s proportionate share of the acquiree’s net assets.

Investments in subsidiaries are accounted for at cost less impairment. Cost is adjusted to reflect changes in consideration arising from contingent consideration amendments. Cost also includes direct attributable costs of investment.

The value of non-controlling interest in equity and the consolidated results are shown, respectively, under 'Non-controlling Interest' of the Consolidated Statement of Financial Position and 'Profit attributable to non-controlling interest from continuing operation" in the Consolidated Income Statement.

Profit for the year and each component of Other comprehensive income is attributed to the owners of the parent and non-controlling interest in accordance with their percentage of ownership. Total Comprehensive income is attributed to the owners of the parent and non-controlling interest even if this results in a debit balance of the latter.

Intercompany transactions and unrealized gains are eliminated and deferred until such gains are realized by the Group, usually through transactions with third parties.

Intercompany balances between entities of the Group included in the consolidation are eliminated during the consolidation process.

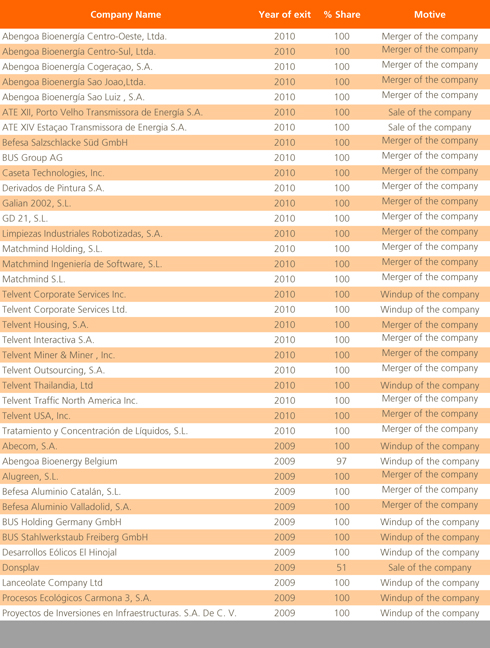

Appendix I and VI of these Consolidated Financial Statements identify the 37 and 63 subsidiaries which were included in the consolidation in 2010 and 2009.

The following table shows those subsidiaries which during 2010 and 2009 were no longer included in the consolidation:

None of these transactions met the qualifying criteria to be classified as discontinued operations.

The aggregated sales and results of 2010 and 2009 of the entities which are no longer consolidated on those years are not significant to the consolidated sales and results.

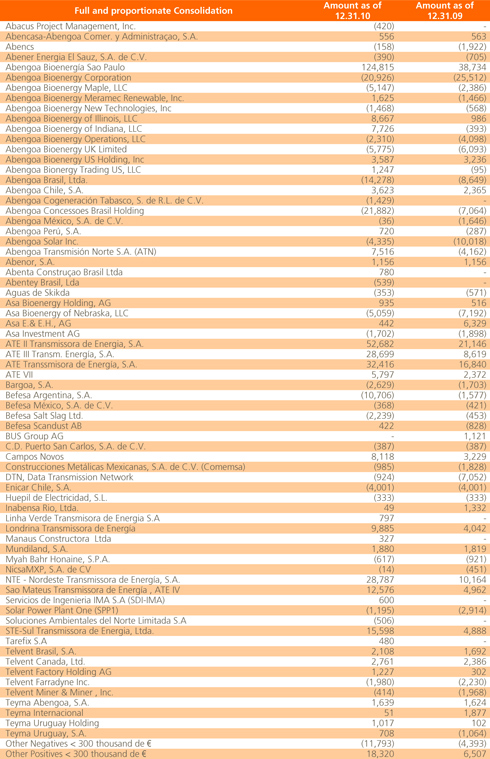

On October 8, 2010, Abengoa concessoes Brasil Holding, S.A., a subsidiary in the Industrial Engineering and Construction segment, closed a purchase agreement, which has been effective on December 31 once the contractual obligations between the parties have been met, at a price of€117 M, for the remaining 49.9% of the company STE Transmissora de Energia, S.A. held by Control y Montajes Industriales - CYMI, S.A. and for 49.99% of the company NTE Transmissora de Energia, S.A. These companies are the operators of two Transmission Lines concessions in Brazil.

At the end of 2010, the price of the agreement remained outstanding and is shown under the “Trade and other payables” heading in the current liabilities. This acquisition did not have a significant impact on Abengoa’s consolidated financial statements at the 2010 year end, since the companies were already being fully consolidated.

On May 27, 2009, Abengoa S.A., through its subsidiary, Telvent Corporation, executed a sales agreement for the sale of 3,576,470 ordinary shares of the company traded on NASDAQ, Telvent GIT S.A., representing 10.49% of the stock. This represented a cash inflow of €45 million and a gain of €16.5 million in 2009.

In addition to the above, on October 28, 2009, Abengoa, S.A. executed another agreement for the sale of 4,192,374 ordinary shares, representing 12.30 % of the stock of Telvent GIT S.A., amounting to a cash inflow of €74 million and a gain of €39.8 million in 2009.

After conclusion of the two aforementioned sale operations, Abengoa, S.A. held 41.09% of the shares of Telvent GIT, S.A. at the 2009 year end Abengoa, S.A. remains the principal shareholder with full de facto control over said company and fully consolidates it as a result of the framework of the relationship between Abengoa, S.A. and Telvent GIT, S.A. This relationship leads to the conclusion that Abengoa, S.A. has the power to govern Telvent’s financial and operating policies in order to obtain profits from its activities, as stated in IAS 27, and, among the evidence used to reach this conclusion, the following may be highlighted:

- the substantial control over the company’s management and control systems;

- the existence of a resolution of the General Meeting of Shareholders, agreeing on the proposal presented by Abengoa, evidences Abengoa's exercise of its "de facto control" over the Company

- the profile and degree of market activity of the other reference shareholders of Telvent, as well as of the shares transactions of such shareholders;

- the company’s free float, the daily trading volume of its shares and the % interest held by Abengoa.

- the absence of agreements between other shareholders;

- the behaviour of other shareholders in line with that of Abengoa at the General Meeting of Shareholders;

- the composition of the Board of Directors and its voting results.

- the structure of the financing and guarantees that Abengoa provides to the company.

In addition, in June 2009, a company reorganization process took place in the Aluminium business area of the Environmental Services business group. This process consisted of a simplified merger of the companies Befesa Aluminio Bilbao (absorbing company), Befesa Aluminio Valladolid (absorbed), Aluminio Catalán (absorbed) and Alugreen (absorbed). The new company resulting from the merger changed its corporate name to Befesa Aluminio, S.L. but kept the registered office and tax identification code of the absorbing company, Befesa Aluminio Bilbao, S.L.

In compliance with Article 155 of Spanish Corporate Law, the parent company has notified to all these companies, either by itself or through another subsidiary, that it owns more than 10 per 100 of their capital.

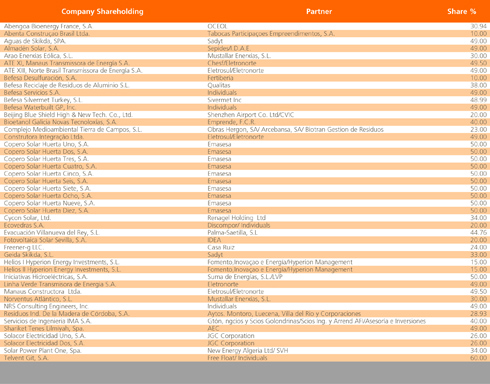

b) Associates

Associates are entities over which Abengoa has a significant influence but does not have control and, generally, involve an interest representing between 20% and 50% of the voting rights. Investments in associates are consolidated by the equity method and are initially recognized at cost. The Group’s investment in associates includes goodwill identified upon acquisition (net of any accumulated impairment loss).

The share in losses or gains after the acquisition of associates is recognized in the Income Statement and the share in movements in reserves subsequent to the acquisition is recognized in the reserves. Movements subsequent to the acquisition are adjusted against the carrying value of the investment. When the share in an associate’s losses is equal to or higher than the interest in the company, including any unsecured accounts receivable, additional losses are not recognized unless Abengoa has acquired any obligations or make any payments in the associate’s name.

Results between the Group and its associates are eliminated to the extent of the Group’s holding in the associate. Additionally, unrealized gains are eliminated, unless the transaction provides evidence of impairment to the asset being transferred. The accounting policies of the associates have been changed where necessary to ensure consistency with the policies adopted by the Group.

In compliance with Article 155 of Spanish Corporate Law, the parent company has notified to all these companies, either by itself or through another subsidiary, that it owns more than 10 per 100 of their capital.

Appendices II and VII of these Accounts set out the details of 3 and 7 entities which in 2010 and 2009, respectively, entered in the consolidation and have been consolidated applying the equity method.

The table below sets out those associate companies which ceased to be associates in the consolidation in 2010 and 2009:

On July 27, 2010, Abengoa concessoes Brasil Holding, S.A., a subsidiary in the Industrial Engineering and Construction segment, concluded an agreement with the company State Grid International to sell its 25% shareholding in the companies ETEE (Expansión Transmisora de Energía Eléctrica, S.A.) and ETIM (Expansión Transmissão Itumbiara Marimbondo), which are responsible for the concession of the 794 kilometers of transmission lines that joins the power stations of the city of Itumbiara, in Soiás, and Marimbondo, in the state of Minas Gerais. The sale of these shareholdings meant a cash inflow of €102 M and a profit of €69 M, recognized under the “Other operating income” epigraph in the consolidated income statement (€45 M after income taxes).The impact upon the Group consolidated results of entities leaving the consolidation as associates was not significant in the years 2010 and 2009.

c) Joint ventures

Joint ventures exist when, by virtue of a contractual arrangement, an entity is jointly managed and owned by Abengoa and third parties outside the Group. These arrangements are based upon an agreement between all the parties that confer to those parties joint control over the financial and operating policies of the entity. Holdings in joint ventures are consolidated using the proportionate method.

The Group consolidates the assets, liabilities, income and expenses, and cash flows of the joint ventures on a line-by-line basis with similar lines in the Group’s accounts.

The Group recognizes its share of gains and losses arising from the sale of Group assets to the joint venture for the portion that relates to other investors. Conversely, the Group does not recognize its share in any gains or losses of the joint venture that result from the purchase of assets from the joint venture by a Group company until those assets have been sold to third parties. Any loss on the transaction is recognized immediately if there is evidence of a reduction in the net realizable value of current assets or an impairment loss. Where necessary, the accounting policies of the joint ventures are adapted so as to ensure consistency with those adopted by the Group.

A business combination involving entities or businesses under common control is a business combination in which all entities or businesses that are combined are controlled, ultimately, by the same party or parties, before and after combination takes place, and this control is not transitory.

When the group experienced a business combination under common control, the assets and liabilities acquired are recorded at the same book amount that were registered previously, and they are not valued at fair value. No goodwill related to the transaction is recognised. Any difference between the purchase price and the net book value of net assets acquired is recognized in equity.

Exhibit III and VIII to the Consolidated Financial Statements identifies the 2 and 4 entities which in 2010 and 2009 have been incorporated in the consolidation.

The consolidation of the joint ventures in 2010 and 2009 did not have a significant effect on the overall consolidated figures at December 2010 and 2009.

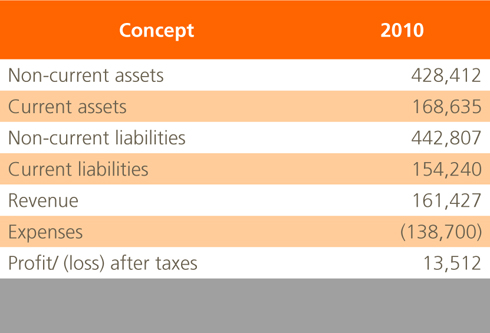

The amounts set out below represent the Group's percentage interest in the assets, liabilities, revenues and profits of the joint ventures in 2010:

There are no contingent liabilities in relation to the Group’s shareholdings in joint ventures, nor contingent liabilities in the joint ventures themselves.

d) Temporary Joint Ventures

Additionally, the group participates in special joint venture arrangements called “Unión Temporal de Empresas” (UTE) in connection with its share of certain long-term construction and service contracts. UTEs are temporary joint ventures generally formed to execute specific commercial and/or industrial projects in a wide variety of areas and particularly in the fields of engineering and construction and infrastructure projects.

They are normally used to combine the characteristics and qualifications of the UTE’s investors into a single proposal in order to obtain the most favorable technical assessment possible.

UTEs are normally limited as standalone entities with limited action, since, although they may enter into commitments in their own name, such commitments are generally undertaken by their investors, in proportion to each investor’s share in the UTE.

The investors’ shares in the UTE normally depend on their contributions (quantitative or qualitative) to the project, are limited to their own tasks and are intended solely to generate their own specific results. Each investor is responsible for executing its own tasks and does so in its own interests, following specific organizational guidelines that comply with the general guidelines coordinated by all the participants in the project.

Overall project management and coordination does not generally extend beyond execution and preparation or presentation of all the technical and financial information and documentation required to carry out the project as a whole. The fact that one of the UTE’s investors acts as project manager does not affect its position or share in the UTE.

The UTE’s investors are collectively responsible for technical issues, although there are strict pari passu clauses that assign the specific consequences of each investor’s correct or incorrect actions.UTEs are not variable-interest or special-purpose entities. UTEs do not usually own assets or liabilities on a standalone basis. Their activity is conducted for a specific period of time that is normally limited to the execution of the project. The UTE may own certain fixed assets used in carrying out its activity, although in this case they are generally acquired and used jointly by all the UTE’s investors, for a period similar to the project’s duration, or prior agreements are reached by the investors regarding the manner and amounts of the assignment or disposal of the UTE’s assets on completion of the project.

The proportional part of the UTE’s Statement of Financial Position and Income Statement is integrated into the Statement of Financial Position and the Income Statement of the participating company in proportion to its interest in the UTE.

There are no contingent liabilities in relation to the Group’s shareholdings in the UTE, nor contingent liabilities in the UTE themselves.

Funds provided by Group companies to the 123 temporary joint ventures excluded from the consolidation (120 in 2009) were €241 thousand (€275 thousand in 2009) and are included under “Financial Investments” in the Consolidated Statement of Financial Position. The net operating profit of the UTEs accounted for 0.69 % of the Group’s consolidated operating profit (0.32% in 2009). The proportional aggregated net profit was €898 thousand (€650 thousand in 2009).

During 2010, a further 61 UTEs (72 in 2009) which commenced their activity and/or have started to undertake a significant level of activity in 2010 or 2009 were included in the consolidation. These UTEs contributed €167,416 thousand (€64,190 thousand in 2009) to the consolidated net sales.

During 2010 40 UTEs (56 in 2009) were excluded from the consolidated group because they had ceased their activities or the latter had become insignificant in relation to overall group activity levels. The proportional consolidated net sales of these UTEs in 2010 were €2,783 thousand (€19,797 thousand in 2009).

There are no contingent liabilities for the Group’s participation in the UTEs and there are no contingent liabilities of the UTEs themselves.

e) Transactions with non-controlling interests

The group treats transactions with non-controlling interests as transactions with equity owners of the group. When the Group acquires non-controlling interests, the difference between any consideration paid and the carrying value of the proportionate share of net assets acquired is recorded in equity. Gains or losses on disposals of non-controlling interests are also recorded in equity.

When the group ceases to have control or significant influence, any retained interest in the entity is remeasured to its fair value, with the change in carrying amount recognized in profit or loss. The fair value is the initial carrying amount for the purposes of subsequently accounting for the retained interest as an associate, joint venture or financial asset. In addition, any amounts previously recognized in other comprehensive income in respect of that entity are accounted for as if the group had directly disposed of the related assets or liabilities. This may mean that amounts previously recognized in other comprehensive income are reclassified to profit or loss.

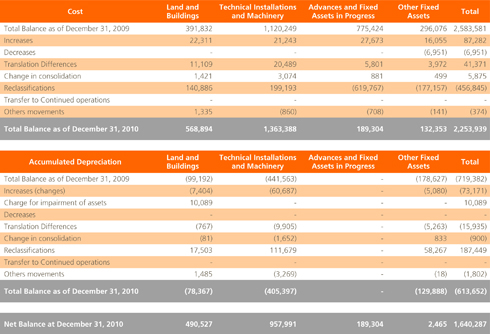

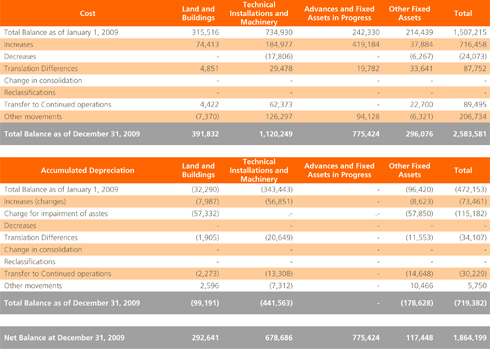

2.3. Property, plant and equipment

2.3.1. Presentation

For the purposes of preparing the Financial Statements, property, plant and equipment has been divided into the following categories:

a) Property, plant and equipment.

b) Property, plant and equipment in Projects.a) Property, plant and equipment

This category includes property, plant and equipment of companies or project companies which has been self-financed or financed through external financing with recourse facilities.

b) Property, plant and equipment in Projects

This category includes property, plant and equipment of companies or project companies which is financed through non-recourse project finance (for further details see Notes 2.4 and 6 on Fixed Assets in Projects).

2.3.2. Measurement

In general, items included within property, plant and equipment are measured at historical cost less depreciation and impairment losses, with the exception of land, which is presented at cost less any impairment losses.

The historical cost includes all expenses directly attributable to the acquisition of property, plant and equipment.

Subsequent costs are capitalized in the asset’s carrying amount or are recognized as a separate asset when it is probable that future economic benefits associated with that asset can be separately and reliably identified.

All other repair and maintenance costs are charged to the Income Statement in the period in which they are incurred.

Work carried out by the Group on its own property, plant and equipment is valued at production cost and is shown as ordinary income in the Income Statement of the company which undertook the work.

In those projects in which the asset is constructed internally by the group and that are not under the scope of IFRIC 12 on service concession agreements (see Note 2.24), the entire intragroup income and expenses are eliminated so that the assets are reflected at their acquisition cost.

In addition, such internal construction projects are capitalized as an increase in the carrying amount of the asset, with regard to both financing obtained specifically for each project and non-project-specific financing from financial institutions. The capitalization of borrowing costs ceases at the moment when, as a result of delays or inefficiencies, the process is either stopped or suspended.

Costs incurred during the construction period may also include gains or losses from foreign-currency cash-flow hedging instruments for the acquisition of property, plant and equipment in foreign currency, which have been transferred directly from equity.

With regard to investments in property, plant and equipment located on land belonging to third parties, an initial estimate of the costs of dismantling the asset and restoring the site to its original condition is also included in the carrying amount of the asset. Such costs are recorded at their net present value in accordance with IAS 37.

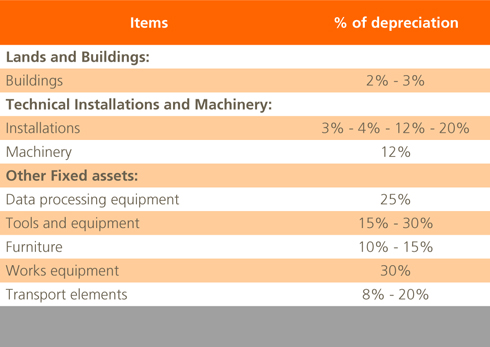

The annual depreciation rates of property, plant and equipment (including property, plant and equipment in projects) are as follows:

Waste ponds and similar assets are depreciated on the basis of the volume of waste in the ponds.

The assets’ residual values and useful economic lives are reviewed, and adjusted if necessary, at the end of the accounting period of the company which owns the asset.

When the carrying amount of an asset is greater than its recoverable amount, the carrying amount is reduced immediately to reflect the lower recoverable amount.

Gains and losses on the disposal of property, plant and equipment, calculated as proceeds received less the asset’s net carrying amount, are recognized in the Consolidated Income Statement, under the line item Other, within the caption Other operating income.

2.4. Fixed assets in projects

This category includes property, plant and equipment and intangible assets of consolidated companies which are financed through non-recourse Project Finance, that are raised specifically and solely to finance individual projects as detailed in the terms of the loan agreement.

These non-recourse Project Finance assets are generally the result of projects which consist of the design, construction, financing, application and maintenance of large-scale complex operational assets or infrastructures, which are owned by the company or are under concession for a period of time. The projects are initially financed through non-recourse medium-term bridge loans and later by non-recourse Project Finance.

In this respect, the basis of the financing agreement between the Company and the bank lies in the allocation of the cash flows generated by the project to the repayment of the principal amount and interest expenses, excluding or limiting the amount secured by other assets, in such a way that the bank recovers the investment solely through the cash flows generated by the project financed, any other debt being subordinated to the debt arising from the non-recourse financing applied to projects until the non-recourse debt has been fully repaid. For this reason, fixed assets in projects are separately reported on the face of the Consolidated Statement of Financial Position, as is the related non-recourse debt in the liability section of the same statement.

In addition, within the fixed assets in projects line item of the Consolidated Statement of Financial Position, assets are sub-classified under the following two sub-headings, depending upon their nature and their accounting treatment:

- Property, plant and equipment: includes tangible fixed assets which are financed through a non-recourse loan and are not subject to a concession agreement as described below. Their accounting treatment is described in Note 2.3.

- Intangible assets: includes fixed assets financed through non-recourse loans, mainly related to service concession agreements, which are accounted for as intangible assets in accordance with IFRIC 12 (see Note 2.24). The rest of the assets shown under this heading are the intangible assets owned by the project company, the description and accounting treatment of which are set forth in Note 2.5.

Non-recourse project finance typically includes the following guarantees:

- Shares of the project developers are pledged.

- Assignment of collection rights.

- Limitations on the availability of assets relating to the project.

- Compliance with debt coverage ratios.

- Subordination of the payment of interest and dividends to meeting these ratios.

Once the project finance has been repaid and the non-recourse debt and related guarantees fully extinguished, assets reported under this category are reclassified to the Property, Plant and Equipment or Intangible Assets line items, as applicable, in the Consolidated Statement of Financial Position.

2.5. Intangible assets

a) Goodwill

Goodwill is recognized as the excess of the sum of the considerations transferred, the amount of any non-controlling interest in the acquire and the fair value, on the date of acquisition, of the previously held interest in the acquiree over the fair value, at the acquisition date, of the identifiable assets acquired and the liabilities and contingent liabilities assumed. If the sum of the considerations transferred, the amount of any non-controlling interest in the acquiree and previously held interest in the acquiree is lower than the fair value of the net assets acquired and it represents a bargain purchase, the difference is recognized directly in the Income Statement.

Goodwill relating to the acquisition of subsidiaries is included in intangible assets, while goodwill relating to associates is included in investments in associates.

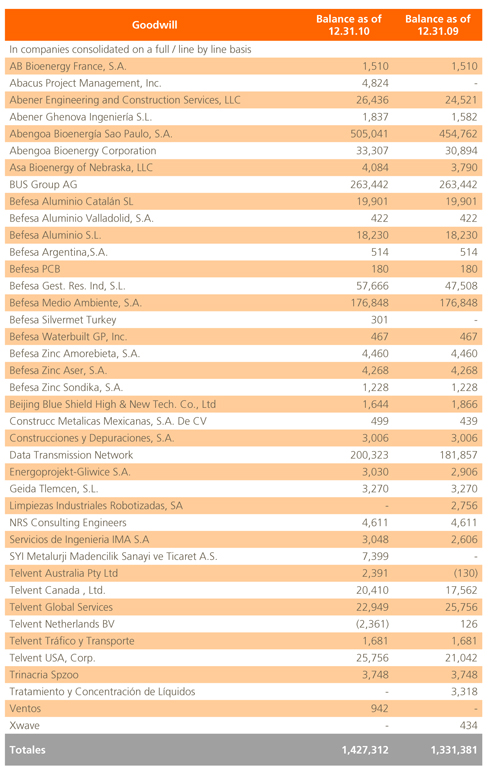

Goodwill is carried at cost less accumulated impairment losses (see Note 2.7). Goodwill is allocated to Cash Generating Units (CGU) for the purposes of impairment testing, these CGU’s being the units which are expected to benefit from the business combination that generated the goodwill.

Gains and losses on disposal of an entity include the carrying amount of goodwill relating to the entity sold.

b) Computer programs

Licenses for computer programs are capitalized on the basis of the original program, comprising purchase costs and preparation/installation cost directly associated with the program. Such costs are amortized over their estimated useful life. Development and maintenance costs are expensed to the Income Statement in the period in which they are incurred.

Costs directly related with the production of identifiable computer programs adapted to the needs of the Group and which are likely to generate economic benefit in excess of their costs for a period of one year are recognized as intangible assets if they fulfill the following conditions:

- It is technically possible to complete the production of intangible asset in such a way that it is available for use or sale;

- Management intends to complete the intangible asset for its use or sale;

- The company is able to use or sell the intangible asset;

- There is availability of appropriate technical, financial or other resources to complete the development and to use or sell the intangible asset; and

- Disbursements attributed to the intangible asset during its development may be reliably measured.

Costs directly related to the production of computer programs recognized as intangible assets are amortized over their estimated useful lives which do not normally exceed 10 years.

Costs that fail to meet the criteria above are recognized as expenses when incurred.

c) Research and development costs

Research costs are recognized as an expense in the period in which they are incurred and they are identified on a project by project basis.

Development costs (relating to the design and testing of new and improved products) are recognized as an intangible asset when all the following criteria are met:

- It is probable that the project will be successful, taking into account its technical and commercial viability, so that the project will be available for its use or sale;

- It is probable that the project will generate future economic benefits, in terms of both external sales or internal use;

- Management intends to complete the project for its use or sale;

- The Company is able to use or sell the intangible asset;

- There is availability of appropriate technical, financial or other resources to complete the development and to use or sell the intangible asset; and

- The costs of the project/product can be estimated reliably.

Once the product is in the market, the capitalized costs are amortized on a straight-line basis over the period for which the product is expected to generate economic benefits, which is normally 5 years, except for development assets related to the thermo-solar plant using tower technology which are amortized over 25 years.

Any other development costs are recognized as an expense in the period in which they are incurred and are not recognized as an asset in later periods.

Grants or subsidized loans obtained to finance research and development projects are recognized in the Income Statement following the rules of capitalization or expensing which have been described above.

d) d) Emission rights of green house gases for own use

This heading recognizes greenhouse gas emissions rights obtained by the Group through allocation by the competent national authority, which are used against the emissions discharged in the course of the Group’s production activities. These emission rights are measured at their cost of acquisition and are derecognized from the Statement of Financial Position when used, under the National Assignation Plan for Greenhouse Gas Permits or when they expire.

Emission rights are tested for impairment to establish whether their acquisition cost is greater than their fair value. If impairment is recognized and, subsequently, the market value of the rights recovers, the impairment loss is reversed through the Income Statement, up to the limit of the original carrying value of the rights.

When emitting greenhouse gases into the atmosphere, the emitting company provides for the tonnage of CO2 emitted at the average purchase price per tonne of rights acquired. Any emissions in excess of the value of the rights purchased in a certain period will give rise to a provision for the cost of the rights at that date.

In the event that the emission right are not for own use but intended to be traded in the market, the contents of Note 2.12 will be applicable.

2.6. Borrowing costs

Borrowing costs incurred in the construction of any qualifying asset are capitalized over the period required to complete and prepare the asset for its intended use (at Abengoa a qualifying asset is defined as an asset for which the production or preparation phase is longer than one year).

Costs incurred relating to non-recourse factoring, when the accounting treatment requires the asset being factored to be derecognized in the Statement of Financial Position, are expensed when the factoring transaction is completed with the financial institution.

Remaining borrowing costs are expensed in the period in which they are incurred.

2.7. Impairment of non-financial assets

On a quarterly basis, Abengoa reviews its property, plant and equipment, intangible assets with finite and indefinite useful life and goodwill to identify any indicators of impairment.

In case any indicator of impairment is identified, Abengoa reviews the asset to determine whether there has been any impairment.

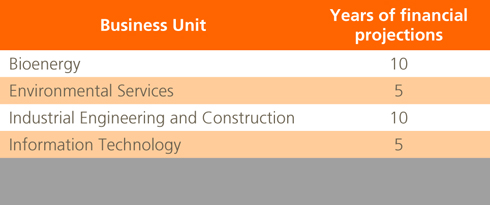

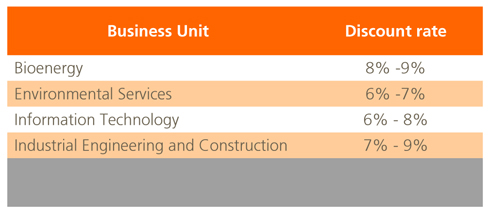

To establish whether there has been any impairment of asset, it is necessary to calculate the asset’s recoverable amount. The recoverable amount is the higher of its market value less costs to sell and the value in use, defined as the present value of the estimated future cash flows to be generated by the asset. In the event that the asset does not generate cash flows independently of other assets, Abengoa calculates the recoverable amount of the Cash-Generating Unit to which the asset belongs. To calculate its value in use, the assumptions include a discount rate, growth rates and projected changes in both selling prices and costs. The discount rate is estimated by the Directors, pre-tax, to reflect both changes in the value of money over time and the risks associated with the specific Cash-Generating Unit. Growth rates and movements in prices and costs are projected based upon internal and industry projections and management experience respectively. Financial projections range between 5 and 10 years depending on the growth potential of each Cash Generating Unit (see Note 4.4.b). The years of financial projections used for the purpose of impairment test for the most significant amounts of goodwill by business unit are disclosed below:

In the event that the recoverable amount of an asset is lower than its carrying amount, an impairment charge for the difference between the recoverable amount and the carrying value of the asset is recorded in the Consolidated Income Statement under the item “Depreciation, amortization and impairment charges”. With the exception of goodwill, impairment losses recognized in prior periods which are later deemed to have been recovered are credited to the same income statement heading.2.8. Financial Investments (current and non-current)

Financial investments are classified into the following categories, based primarily on the purpose for which they were acquired:

a) Financial assets at fair value through profit and loss;

b) Loans and receivables;

c) Financial assets held to maturity; and

d) Financial assets available for sale.

Management determines the classification of each financial asset upon initial recognition, with their classification subsequently being reviewed at each year end.

a) Financial assets at fair value through profit and loss

This category includes the financial assets acquired for trading and those initially designated at fair value through profit and loss. A financial asset is classified in this category if it is acquired mainly for the purpose of sale in the short term or if it is so designated by Management. Financial derivates are also classified as acquired for trading unless they are designated as hedging instruments. The assets of this category are classified as current assets, if they are expected to be realized in less than 12 months after the year-end date of each company. Otherwise, they are classified as non-current assets.

These financial assets are recognized initially at fair value, without including transaction costs. Subsequent changes in fair value of the assets are recognized under “Gains or losses from financial assets at fair value” within the “Finance income or expense” line of the Income Statement for the period.

b) Accounts receivable

Loans and receivables are considered to be non-derivative financial assets with fixed or determinable payments which are not listed on an active market. They are included as current assets except in cases in which they mature more than 12 months after the date of the Statement of Financial Position.

Following the application of IFRIC 12, certain assets under concession can qualify as financial receivables (see Note 2.24).

Loans and receivables are initially recognized at fair value plus transaction costs. Subsequently to their initial recognition, loans and receivables are measured at amortized costs in accordance with the effective interest rate method. Interest calculated using the effective interest rate method is recognized under “Interest income from loans and debts” within the “Other net finance income/expense” line of the Income Statement.

c) Financial assets held to maturity

This category includes those financial assets which are expected to be held to maturity and which and are not derivatives and have fixed or determinable payments.

These assets are initially recognized at fair value plus transaction costs and subsequently at their amortized cost under the effective interest rate method. Interest calculated under the effective interest rate method is recognized under “Other finance income” within the “Other net finance income/expense” line of the Income Statement”.

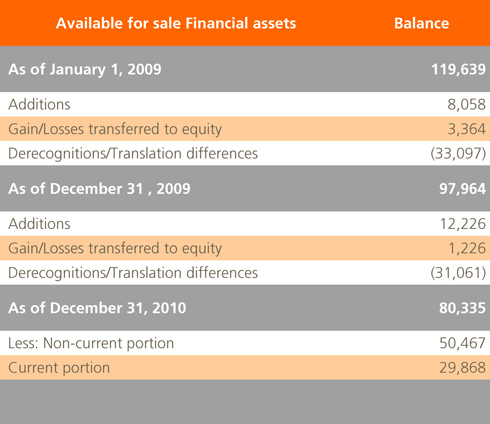

d) Financial assets available-for-sale

This category includes non-derivative financial assets which do not fall within any of the previously mentioned categories. For Abengoa, they primarily comprise interests in other companies that are not consolidated. They are classified as non-current assets, unless Management anticipates the disposal of such investments within 12 months following the date of the company’s Statement of Financial Position.

Financial assets available for sale are recognized initially at fair value plus transaction costs. Subsequent changes in the fair value of these financial assets are recognized directly in equity, with the exception of translation differences of monetary assets, which are charged to the Income Statement. Dividends from available-for-sale financial assets are recognized under “Other finance income” within the “Other net finance income/expense” line of the Income Statement when the right to receive the dividend is established.

When available-for-sale financial assets are sold or are impaired, the accumulated amount recorded in equity is transferred to the Income Statement. The amount of the cumulative loss that is reclassified from equity to profit or loss in cases when the financial assets are impaired is the difference between the acquisition cost (net of any principal repayment and amortization) and current fair value, less any impairment loss on that financial asset previously recognized in profit or loss To establish whether the assets have been impaired, it is necessary to consider whether the reduction in their fair value is significantly below cost and whether it will be for a prolonged period of time. The accumulated loss is the difference between the acquisition cost and the fair value less any impairment losses. In general, impairment losses recognized in the Income Statement are not later reversed through the Income Statement.

Acquisitions and disposals of financial assets are recognized on the trading date, i.e. the date upon which there is a commitment to purchase or sell the asset. The investments are derecognized when the right to received cash flows from the investment has expired or has been transferred and all the risks and rewards derived from owning the asset have likewise been substantially transferred.

The fair value of listed financial assets is based upon current purchase prices. If the market for a given financial asset is not active (and for assets which are not listed), the fair value is established using valuation techniques such as considering recent free market transactions between interested and knowledgeable parties, in relation to other substantially similar instruments, analyzing discounted cash flows and option price fixing models, using to the greatest extent possible, information available in the market.

At the date of each Statement of Financial Position, the Group evaluates if there is any objective evidence that the value of any financial asset or any group of financial assets has been impaired.

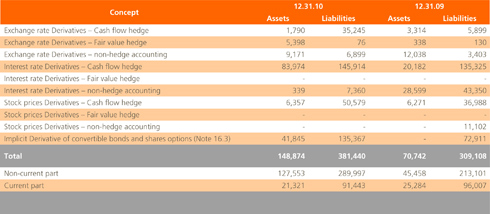

2.9. Derivative financial instruments and hedging activities

Derivatives are initially recognized at fair value on the date that the derivative contract is entered into, and are subsequently measured at fair value. The basis for recognizing the gain or loss from changes in the fair value of the derivative depends upon whether the derivative is designated as a hedging instrument and, if so, the nature of the item being hedged.

The relationship between hedging instruments and hedged items is documented at the beginning of each transaction, as well as its objectives for risk management and strategy for undertaking various hedge transactions.

Both the start of the hedge and subsequently on a continual basis at each closing an effectiveness test is performed on each of the derivative financial instruments designated as a hedge to justify being offset against changes in the fair value or cash flows relating to the hedged items.

The most common methods that have been chosen by the Group to measure the effectiveness of financial instruments designated to be hedges, are the dollar offset and regression methods.

Either of these methods are applied by the Group to perform the following effectiveness tests:

- Prospective effectiveness test: performed at the designation date and at each accounting closing date for the purposes of determining that the hedge relationship continues to be effective and can be designated in the subsequent period.

- Retrospective effectiveness test: performed at each accounting closing date in order to determine the ineffectiveness of the hedge, which must be recognized in the income statement.

At the inception of each transaction, the Group documents the relationship between the hedging instrument and the item being hedged as well as its risk management objectives and the strategy for undertaking the different hedging transactions. The Group also documents its assessment, both at hedge inception and on an ongoing basis, of whether the derivatives that are used in hedging transactions are effective in offsetting changes in the fair value or cash flows of the hedged items.

On this basis there are three types of derivative:

a) Fair value hedge for recognized assets and liabilities

Changes in fair value are recorded in the Income Statement, together with any changes in the fair value of the asset or liability that is being hedged.

b) Cash flow hedge for forecast transactions

The effective portion of a change in the fair value of derivatives is recognized in equity, whilst the gain or loss relating to the ineffective portion is recognized immediately in the consolidated Income Statement.

However, when designating a one-side risk as a hedged risk the intrinsic value and time value of the financial hedge instrument are separated, recording the changes in the intrinsic value on equity, while changes in the time value are recorded in the Consolidated Income Statement. The Group has financial hedge instruments with these characteristics, such as interest rate options (caps), which are described in Note 11.

Amounts accumulated in equity are transferred to the Income Statement in periods in which the hedged item impacts profit and loss. However, when the forecast transaction which is hedged results in the recognition of a non-financial asset or liability, the gains and losses previously deferred in equity are included in the initial measurement of the cost of the asset or liability.

When the hedging instrument matures or is sold, or when it no longer meets the criteria required for hedge accounting, accumulated gains and losses recorded in equity remain as such until the forecast transaction is ultimately recognized in the Income Statement. However, if it becomes unlikely that the forecast transaction will actually take place, the accumulated gains and losses in equity are recognized immediately in the Income Statement.

c) Net investment hedges

Hedges of a net investment in a foreign operation, including the hedging of a monetary item considered part of a net investment, are recognized in a similar way to cash flow hedges:

- The part of the loss or gain of the hedging instrument that is determined to be an effective hedge is directly recognized in equity (see IAS 1), and

- The part that is ineffective is recognized in the Income Statement of the year.

The profit or loss of the hedging instrument in relation to the part of the hedge that is directly recognized in equity is recognized in the Income Statement for the year when the foreign operation is sold or disposed of.

The total fair value of hedging instruments is recorded as a non-current asset or liability when the hedged item is to mature at more than 12 months and as a current asset or liability if less than 12 months. Trading derivatives are classified as a current asset or liability.

Changes in the fair value of derivative instruments which do not qualify for hedge accounting are recognized immediately in the Income Statement.

Contracts held for the purposes of receiving or making payment of non-financial elements in accordance with expected purchases, sales or use of goods (“own-use contracts”) of the Group are not recognized as derivative instruments, but as executory contracts. In the event that such contracts include embedded derivatives, they are recognized separately from the host contract, if the economic characteristics of the embedded derivative are not closely related to the economic characteristics of the host contract. The options contracted for the purchase or sale of non-financial elements which may be cancelled through cash outflows are not considered to be own-use contracts.

2.10. Fair value estimates

The fair value of financial instruments which are traded on active markets (such as officially listed derivatives, investments acquired for trading and available-for-sale instruments) is determined by the market value as at the date of the Statement of Financial Position.

A market is considered active when quoted prices are readily and regularly available from stock markets, financial intermediaries, among others, and these prices reflect current market transactions regularly occur between parties that operate independently.

The fair value of financial instruments which are not listed and do not have a readily available market value is determined by applying various valuation techniques and through assumptions based upon market conditions as of the date of the Statement of Financial Position. For long-term debt, the market prices of similar instruments are applied. For the remaining financial instruments, other techniques are used such as calculating the present value of estimated future cash flows. The fair value of interest rate swaps is calculated as the present value of estimated future cash flows. The fair value of forward exchange rate contracts is measured on the basis of market forward exchange rates as at the date of Statement of Financial Position.

The nominal value of receivables and payables less estimated impairment adjustments is assumed to be similar to their fair value due to their short-term nature. The fair value of financial liabilities is estimated as the present value of contractual future cash outflows, using market interest rate available to the Group for similar financial instruments.

Detailed information on fair values is included in Note 9.2.

2.11. Inventories

Inventories are stated at the lower of cost or net realizable value. In general, cost is determined by using the first-in-first-out (FIFO) method. The cost of finished goods and work in progress includes design costs, raw materials, direct labor, other direct costs and general manufacturing costs (assuming normal operating capacity). Borrowing costs are not included. The net realizable value is the estimated sales value in the normal course of business, less applicable variable selling costs.

Cost of inventories includes the transfer from equity of gains and losses on qualifying cash-flow hedging instruments related with the purchase of raw materials or with foreign exchange contracts.

2.12. Carbon emission credits (CERs)

Several Abengoa entities are involved in a number of external projects to reduce CO2 emissions through participation in Clean Development Mechanisms (CDM) and Joint Implementation (JI) programs with those countries/parties which are purchasing Carbon Emission Credits (CERs) and Emission Reduction Credits (ERUs), respectively. CDMs are projects in countries which are not required to reduce emission levels, whilst JIs are aimed at developing countries which are required to reduce emissions.

Both projects are developed in two phases:

1) Development phase, which, in turn, has the following stages:

Thus, the Group currently holds various agreements for consultancy services within the framework of the execution of Clean Development Mechanisms (CDM). Costs incurred in connection with such consultancy services are recognized by the Group as non-current receivables.

2) Phase of annual verification of the reductions in CO2 emissions. After this verification, the company receives Carbon Emission Credits (CERs), which are registered in the National Register of Emission Rights. CERs are recorded as inventories and measured at market value.

Likewise, the company may hold Emission Allowances assigned by the competent EU Emission Allowance Authority (EUAs), which may also be measured at market price if held for sale. In the event that the EUA are held for own use (see Note 2.5.b).

Furthermore, there are carbon fund holdings aimed at financing the acquisition of emissions from projects which contribute to a reduction in greenhouse gas emissions in developing countries through CDM’s and JA’s, as discussed above. Certain Abengoa companies have holdings in such carbon reduction funds which are managed by an external Fund Management team. The Fund directs the resources of the funds to purchasing Emission Reductions through MDL and AC projects.

The company with holdings in the fund incurs a number costs (ownership commissions, prepayments and purchases of CER’s). From the start, the holding is recorded [on the balance sheet based upon the original Carbon Emission Credit (CER) allocation agreement; however this amount will be allocated over the life of the fund. The price of the CER is fixed for each ERPA. Based upon its percentage holding, and on the fixed Price of the CER, it receives a number of CER’s as obtained by the Fund from each project.

These contributions are considered as long-term investments and are recognized in the Consolidated Financial Statement under the heading of Other Financial Investments.

2.13. Biological assets