Annual Report 2010

- Corporate Governance

- Annual Report on Corporate Governance

- Other Information of Interest

G - Other information of interest

If you consider that there is any material aspect or principle relating to the Corporate Governance practices followed by your company that has not been addressed in this report, indicate and explain below.

First annex:

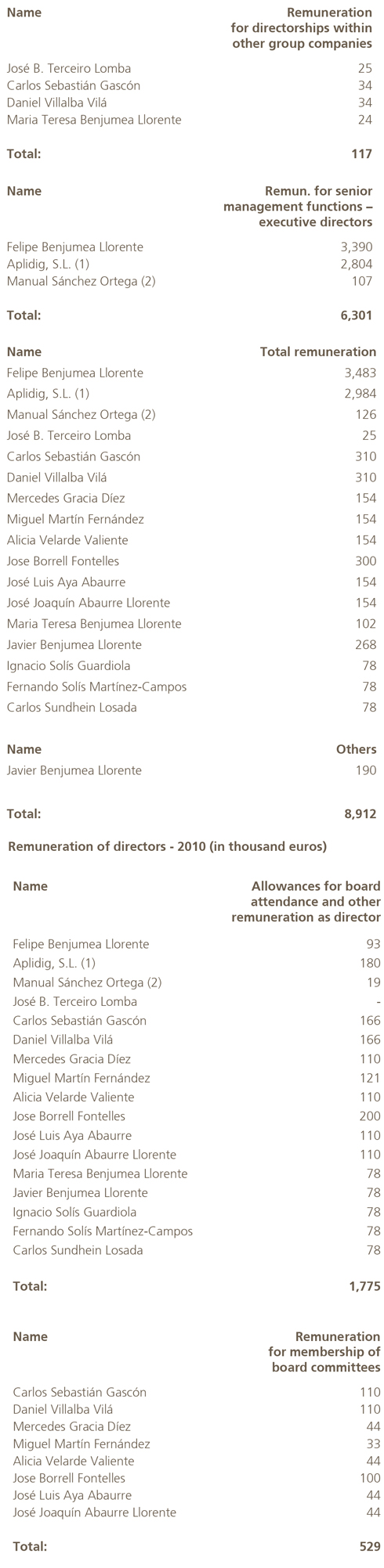

A table detailing the individual remuneration of directors is attached hereto as complementary information to section B.1.11 and following.

(1) Represented by José B. Terceiro/Aplidig SL

(2) From 25/10/2010

Comparing directors’ salary in 2009 and 2010 (8.7 M € in 2009 and 8.9 M € in 2010), it is concluded that a 2.2% has been applied in its total value.

Second annex:

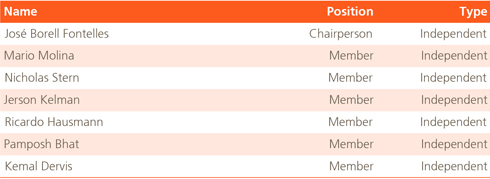

International Advisory Board

Abengoa has created an international Advisory Board that consists of a maximum of nine members. Only the Board of Directors is empowered to elect them and appoint its chairperson. It will act of secretary the Technical General Secretary of Abengoa.

The Advisory Committee is a non-ruled voluntary body that renders technical and advisory consultancy services to the Board of Directors, to which it is organically and functionally subordinate, as consultant and strictly professional adviser; its main function is to serve as support to the Board of Directors within the scope of the latter’s own competences, collaborating and advising, basically focusing its activities on responding to enquiries made by the Board of Directors in connection to all issues that the Board of Directors may enquire on or even raising proposals deemed outcome of their experience and analysis.

Its current composition is as follows:

Tirth annex:

The Internal Code of Conduct in Stock Markets was instituted in August 2007 and it is applicable to all administrators, to the Strategy Committee members and to some employees depending on the activity they develop and the information to which they may have access.

It establishes the obligation to safeguard the information and to protect the confidentiality of relevant facts in the stages prior to decision and publication, as well as establishing the procedure for maintaining internal and external confidentiality, the shares ownership registry, stock operations and interest conflicts.

The secretary general is in charge of monitoring and supervision. It’s available at www.abengoa.com.

Fourth annex:

D.4 Identification and description of the processes for complying with the different regulations that affect the company and/or its group.

In February 2010, the National Stock Market Commission published the document “Internal Control over Financial Reporting in Listed Entities”, which contains two new legal obligations that listed companies must meet from 2011 onwards:

- The audit committees will be responsible for supervising the financial reporting and the efficiency of the company’s internal control and risk management systems.

- Companies will have to inform the markets of their systems of internal control over financial reporting through the Annual Corporate Governance Report.

The National Stock Market Commission’s document is based on COSO and includes 30 recommended practices divided into five components:

- Internal Control Environment

- Financial Reporting Risk Assessment

- Control Activities

- Information and Communication, and

- System Operation Supervision

Since 2007, Abengoa has voluntarily submitted its Internal Control Systems to external evaluation, with the issuance of an audit opinion under PCAOB standards and a compliance audit under section 404 of the Sarbanes-Oxley Act (SOX).

This fact implies that Abengoa has been complying strictly with the reference indicators included in the National Stock Market Commission’s “Systems of Internal Control over Financial Reporting” document for four financial years.

The conceptual framework used as a reference is the COSO model, since it is the model that is closest to the approach required by SOX, which has also been presented to the Audit Committee. In this model, internal control is defined as the process carried out in order to provide reasonable assurance of the attainment of certain objectives, such as compliance with laws and regulations, the reliability of financial reporting and the effectiveness and efficiency of operations.

I) Internal Audit service

In order to supervise the sufficiency, suitability and efficient working of the internal control and risk management systems, the Committee received regular information in 2010 from the person responsible for Corporate Internal Audit in relation to:

- The Annual Internal Audit Plan and the degree to which it had been met.

- The degree of implementation of the recommendations issued.

- Other more detailed explanations which the Audit Committee had requested.

One factor that had a decisive effect on the number of recommendations issued was the performance of internal control compliance audits under PCAOB (Public Accounting Oversight Board) standards, in accordance with the requirements of section 404 of the Sarbanes-Oxley Act (SOX).

I. i) The Internal Audit service in Abengoa

The Internal Audit service originated as an independent global function, reporting to the Audit Committee of the Board of Directors, with the principal objective of supervising Abengoa’s internal control and significant risk management systems.

I. ii) Structure and Team

Abengoa’s Internal Audit service is structured around the joint audit services, which act in coordination. To meet its functions and carry on its activities, it has a structure based on multidisciplinary teams, formally organized by geographical area, which work under a sole Annual Plan of activities and share execution of the tasks on the basis of their qualifications, applying the best international practices.

I. iii). General Objectives

Objectives of the Internal Audit Service:

Forestalling the audit risks to which group companies, projects and activities are exposed, such as fraud, capital losses, operational inefficiencies and, in general, any risks that may affect the healthy running of the business.

Controlling the manner in which the corporate Common Management Systems are applied.

To create value for Abengoa and its Business Groups, promoting the creation of synergies and the monitoring of optimal management practices.

To coordinate the criteria and focuses for the work with the external auditors, seeking the greatest efficiency and profitability of the two functions.

Analysis and processing of the complaints received and notification of the work performed to the Audit Committee.

To evaluate the companies’ audit risk following an objective procedure.

To develop the Work Plans with the appropriate scopes for each different situation.

I. iv). Evaluation of the Internal Audit Service

In 2010, Abengoa commenced a process for the independent evaluation of the Audit service in accordance with the standards of the Institute of Internal Auditors.

The objective of the evaluation of the Internal Audit Service is to assess organization, processes and performance in the internal audit field, in order to fix the parameters to improve the Audit Service’s effectiveness and efficiency and thus deal with an increasingly demanding competitive and regulatory environment.

II) External Audit

The auditor of the individual and consolidated annual financial statements of Abengoa, S.A. is PricewaterhouseCoopers, which is also the Group’s main auditor.

The Audit Committee proposed the appointment of this firm to the Board of Directors, in order for the latter to subsequently submit it to the General Meeting of Shareholders, due to said firm’s extensive knowledge of the Group and its history, which were valued very favorably by both the Committee itself and Management.

Notwithstanding, a significant part of the Group, basically the Information Technologies Business Group (Telvent), is audited by Deloitte.

In addition, other firms collaborate in performing the audit, especially in small companies, both in Spain and abroad, although their scope is not significant in the Group overall.

The Audit Committee’s functions include ensuring the independence of the external auditor, proposing the appointment or renewal thereof to the Board of Directors and approving its fees.

II. i) Planning of the External Audit:

To familiarize itself with the external audit plan.

To understand what the company expects from the auditor: type of service, timeframes and information requirements.

To examine the experience of the audit teams.

To appreciate that the main areas of risk will be tackled during the audit.

SOX (Sarbanes-Oxley Act) internal control audit work is assigned to the same firms following the same criterion, since, according to PCAOB (Public Accounting Oversight Board) rules, the firm that issues the opinion on the financial statements must also be the firm that evaluates the internal control over the preparation of these statements, since this internal control is a key factor in “integrated audits”.

Abengoa follows the policy of having an external audit performed on all group companies, even if they are not obliged to do so because they do not meet the legal requirements.

A total of 46 new companies have been audited this year, more than 85% of which are being audited by one of the four main international audit firms or “Big Four.

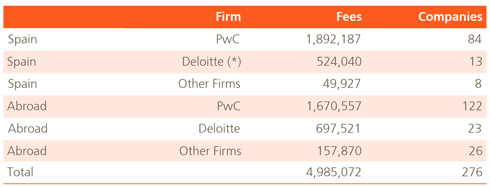

The global fees agreed with the external auditors for the 2010 audit, including the review of regular reporting, the audit of the company listed in the USA under US GAAP and the SOX audit, together with the distribution thereof, is shown below:

(*) Includes, among others, the fees for the quarterly review of the financial statements of the listed subsidiary in the USA under US GAAP.

When assigning work other than the financial audit to any of the “Big Four” audit firms, the company has a prior verification procedure, in order to detect the existence of possible incompatibilities that would prevent the firm from performing the work under the rules of the SEC (Securities Exchange Commission) or ICAC (Instituto de Contabilidad y Auditoría de Cuentas).

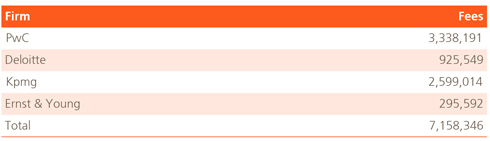

The amount of the fees incurred with the four main audit firms for work other than the financial audit in the year 2010 is shown in the following chart:

(*) Includes 1,249,500 € for other supplementary audit services provided by the main auditor in accordance with the requirements of current legislation.

When thus required, the external auditor has attended Audit Committee meetings to report on its areas of competency, which are basically the following.

- Review of the financial statements of the consolidated group and its companies and issuing an audit opinion thereon.

Although the auditors must issue their opinion on the financial statements as of December 31 each year, the work they conduct in each of the companies includes a review as of an earlier date, which is usually the end of the third quarter (September), in order to anticipate any significant transactions or other matters that have arisen up to said date.

Since the year 2008, Abengoa and its listed subsidiaries voluntarily submit their six-monthly statements to a limited review, issued by the relevant auditor.

Furthermore, reviews are conducted of the quarterly statements prepared in order to provide the financial reporting required by official bodies.

Likewise, the consolidated financial statements of each one of the five Business Groups: Abeinsa, Befesa, Telvent GIT, Abengoa Bioenergía and Abengoa Solar, are audited.

- Evaluation of the internal control system and issuance of an audit opinion under PCAOB (Public Company Accounting Oversight Board) standards, (SOX -Sarbanes-Oxley Act- compliance).

The specific PCAOB rules involve the performance of a series of additional audit procedures. The SEC (Securities Exchange Commission) delegates to the PCAOB the preparation and issuance of the standards to be met by the external auditors in the course of their evaluation of internal control in an integrated audit.

In 2010, the external auditors carried out an integrated audit under PCAOB standards.

As a result of this work, the external auditors likewise issued a report with the conclusions of the internal control evaluation. This opinion is additional to the opinion included in the audit report on the annual financial statements, although the PCAOB allows both opinions to be included in the same document.

II. i) Matters of special interest

For certain matters or specific or significant transactions, the external auditor is required to provide its opinion on the criteria adopted by the company, in order to reach a consensus.

II. ii) Independent Verification Reports prepared by external auditors

One of the axes of the company’s strategy is its commitment to transparency and meticulousness. To reinforce this commitment, some years ago, the company fixed the objective that all the information that appears in the Annual Report should be verified externally.

Thus, in the year 2007, the company submitted the Corporate Social Responsibility Report to verification for the first time. In the year 2008, it was the Report on Greenhouse Gas Emissions and, in 2009 the Corporate Governance Report was verified externally.

Thus, in the year 2010, 6 reports were issued by the external auditors and form an integral part of the Annual Report:

- Audit report on the Group’s consolidated financial statements, as required by current legislation.

- Voluntary audit report on internal audit compliance under PCAOB (Public Company Accounting Oversight Board) standards, as required under section 404 of the Sarbanes-Oxley Act (SOX).

- Voluntary reasonable assurance verification report on the Corporate Governance Report, being the first Spanish listed company to obtain a report of this kind.

- Voluntary reasonable assurance verification report on the Corporate Social Responsibility Report.

- Voluntary verification report on the inventory of greenhouse gas emissions.

- Voluntary verification report on the design of the Risk Management System in accordance with the specifications of ISO 31000.

III) Internal Control

The Audit Committee’s main objectives concerning internal control over the preparation of the financial reporting are:

- To determine the risks of a possible material error in the financial reporting caused by fraud or possible fraud risk factors.

- Analysis of the procedures to assess the efficiency of internal control in relation to the financial reporting.

- Capacity of the internal controls over the processes that affect Abengoa and its Business Groups.

- To identify the material deficiencies and weaknesses in the internal control in relation to the financial reporting and the response capacity.

- To supervise and coordinate any significant changes made over the internal controls related to the quarterly financial reporting.

- Performance of the quarterly processes of closing the financial statements and differences identified in relation to the processes performed at the year end.

- Putting in place plans and monitoring for the actions implemented to correct the differences identified in the audits.

- Measures to identify and correct possible internal control weaknesses in relation to the financial reporting.

- Analysis of procedures, activities and controls that seek to guarantee the reliability of the financial reporting and prevent fraud.

III i) Complaints Channel

Abengoa and its different Business Groups employ a mechanism for complaints to the Audit Committee, which was formally put in place in the year 2007 under the requirements of the Sarbanes-Oxley Act.

Abengoa has two complaint channels:

- An internal channel, which is available to all employees, so that they can notify any alleged irregularity in accounting or audit or breaches of the Code of Conduct. The communication channel is by e-mail or ordinary mail.

- An external cannel, available to anyone outside the company, so that they can notify any alleged irregularities, fraudulent actions or breaches of Abengoa’s Code of Conduct through the web page (www.abengoa.com).

With the creation of these channels, Abengoa has wished to provide a specific method of communication with Management and the governing bodies, which may be used as a tool to inform them of any possible irregularity, non-compliance, unethical or illegal conduct or breach of the rules that govern the Group.

III. ii) Supervision and Control of the Risk Management Model at Abengoa

Abengoa’s Risk Management Model comprises two basic elements:

Business Risks and Risks Associated with the Reliability of Financial Information. The former are covered by the Common Management Systems and the latter by the Compulsory Procedures (SOX)

These two elements form an integrated system that allows appropriate risk management and control at all levels of the organization.

III. iii) Common Management Systems

The Common Management Systems represent the internal rules of Abengoa and all its Business Groups and their method of assessing and controlling risks. They represent a common culture in the management of Abengoa’s businesses, sharing the knowledge accumulated and fixing criteria and guidelines for action.

The Common Management Systems include specific procedures that cover any action that may result in either an economic or non-economic risk for the organization. Furthermore, they are available to all employees en electronic format, irrespective of their geographical location or job.

The CMS must verify and certify compliance with these procedures. This annual certification is issued by the Audit Committee in January of the following year.

The Systems cover the whole organization at three levels:

- All the Business Groups and areas of activity;

- All levels of responsibility;

- All kinds of operations.

Our Common Management Systems represent a common culture for Abengoa’s different businesses and are composed of eleven Rules defining how each one of the potential risks included in Abengoa’s risk model should be managed. Through these systems, the risks and the appropriate way to cover them are identified and the control mechanisms are defined.

Over recent years, the Common Management Systems have evolved to adapt to the new situations and environments in which Abengoa operates, with the principal intention of reinforcing risk identification, covering the risks and fixing control activities.

III. iv) Compulsory Procedures (SOX)

The Compulsory Procedures are used to mitigate the risks relating to the reliability of the financial reporting, by means of a combined system of procedures and control activities in key areas of the company, which are intended to ensure the reliability of the financial reporting and avoid fraud.

As a result of our commitment to transparency, in order to continue to ensure the reliability of the financial reporting prepared by the company, we have continued to reinforce our internal control structure, adapting it to the requirements established in section 404 of the United States Sarbanes-Oxley Act (SOX). For a further year, we have wished to voluntarily submit the internal control system of the whole group to an independent evaluation process conducted by external auditors under the PCAOB (Public Company Accounting Oversight Board) audit standards.

SOX is a compulsory law for all companies listed in the United States and is intended to ensure the reliability of the financial reporting of these companies and protect the interests of their shareholders and investors by setting up an appropriate internal control system. Thus, although only one of the Business Groups –Information Technologies (Telvent)- is obliged to meet SOX requirements, Abengoa deems it necessary to meet these requirements both in the subsidiary that is listed in the United States and in the rest of the companies, since these requirements complete the risk control model used by the company.

- An appropriate internal control system is in place and uses three tools:

- A description of the company’s relevant processes that have a potential impact on the financial reporting that is prepared.

In this respect, 41 Management Processes (MPs) have been identified and grouped into Corporate Cycles and Cycles Common to the Business Groups.

- A series of flow charts that provide a visual description of the processes.

- An inventory of the control activities in each process that ensures attainment of the control objectives.

At Abengoa, we have seen this legal requirement as an opportunity for improvement and, far from being satisfied with the rules included in the Act, have tried to develop our internal control structures, the control procedures and the evaluation procedures applied to a maximum.

This initiative arose in response to the swift expansion undergone by the Group in recent years and future growth expectations, in order to enable us to continue to guarantee the preparation of accurate, timely and complete financial reports to our investors.

In order to meet the requirements of section 404 of the SOX, Abengoa’s internal control structure has been redefined following a “Top-Down” approach based on risk analysis.

Said risk analysis covers the initial identification of significant risk areas and the evaluation of the controls that the company has in place over them, starting with those executed at the highest level –corporate and supervisory controls-, then dropping to the operational controls present in each process.

IV) Risk Management

Abengoa is aware of the importance of managing its risks in order to carry out appropriate strategic planning and attain the defined business objectives. To do this, it applies a philosophy formed by a set of shared beliefs and attitudes, which define how risk is considered, starting with the development and implementation of the strategy and ending with the day-to-day activities.

The risk management philosophy is set out and applied through Abengoa’s Risk Management System, which is completed with the Universal Risk Model. Abengoa’s Risk Management System is shown in the following diagram:

Abengoa defines risk as any potential event that may prevent the company from reaching its business objectives. Abengoa considers that a risk arises as a loss of opportunities and/or strengths or the materialization of a threat and/or strengthening of a weakness.

Abengoa’s attitude in the face of risk is awareness, involvement and anticipation. The key principles of Risk Management at Abengoa are the following:

- In order to attain the business objectives fixed, risks must be managed at all levels of the company without exception.

- Risk Management includes the identification and assessment of, response to, monitoring or follow-up of and reporting of risks in accordance with the procedures in place for these purposes.

- Responses to risks must be consist and must be well adapted to the conditions of the business and the economic environment.

- Management must regularly evaluate the assessment of its risks and the responses that have been designed.

- Monitoring will be conducted regularly and the conformity of the activities of identification, assessment, response, monitoring and reporting included in Abengoa’s Risk Management System will be reported.

IV. i) The Universal Risk Model

Abengoa’s Universal Risk Model is made up of four categories, twenty subcategories and a total of 94 principal risks for the business. Each one of these risks has an associated series of indicators that allow its probability and impact to be measured and the degree of tolerance of the risk to be defined.

For each risk, at least one probability indicator and an impact indicator have been established. These may be quantitative and/or semi-quantitative indicators, while, at the same time, they allow tolerance levels to be fixed for subsequent evaluation and monitoring.

As a result of the assignation of probability and impact indicators to all the risks that form Abengoa’s Universal Risk Model, the risks are classified into four types, each of which has a predetermined risk strategy:

Minor Risk: risks that occur frequently but have little economic impact. These risks are managed to reduce their frequency only if managing them is economically viable.

Tolerable Risk: risks that occur infrequently and have little economic impact. These risks are monitored to check that they are still tolerable.

Severe Risk: frequent risk with a very strong impact. These risks are managed immediately, although, due to the Risk Management processes implemented by Abengoa, it is unlikely that Abengoa needs to tackle this type of risk.

Critical or Emerging Risk: risks that occur infrequently but have a very high economic impact.

Fifth annex:

Abengoa and its business groups have been operating a whistleblower channel since 2007 pursuant to the requirements of the Sarbanes-Oxley Act, whereby interested parties may report to the Audit Committee possible irregular practices concerning accounting, auditing or internal controls over financial reporting. A register is kept of all communications received in relation to the whistleblower, subject to the necessary guarantees of confidentiality, integrity

and availability of the information. The internal audit team conducts an inquiry into each claim it receives.

In cases that involve highly technical matters, the company secures the assistance of independent experts, thus ensuring at all times that it has the sufficient means of conducting a thorough investigation and guaranteeing sufficient levels of objectivity when performing the work.

Within this section, you may include any other information, clarification or detail related to the above sections of the report, to the extent that these are deemed relevant and not reiterative.

Specifically, indicate whether the company is subject to non-Spanish legislation with regard to corporate governance and, if so, include the information it is obliged to provide and which is different from that required in this report.

Binding definition of independent director:

List any Independent Directors who maintain, or have maintained in the past, a relationship with the company, its significant shareholders or managers, when the significance or importance thereof would dictate that the directors in question may not be considered independent pursuant to the definition thereof set forth in section 5 of the Unified Good Governance Code:

No

Date and signature:

This annual corporate governance report was approved by the company’s Board of Directors at its meeting held on:

23/02/2010

Indicate whether there were any directors who voted against or abstained in relation to the approval of this report.

No